First COVID-19, now Small Brewers Duty threshold reform, where next for the Craft Brewery sector?

Perhaps a new era and form of collaboration/consolidation?

An already precarious business outlook for many small breweries across the UK, who had just about boxed and weaved their way through the impact of Covid 19 were dealt a potentially fatal blow from the proposed change in the Small Brewers Duty regime in late July, with the added uncertainly of an increasingly likely ‘no deal’ Brexit also looming.

The news released on 21st July that the UK Government had decided to reduce the threshold at which Small Brewers Duty Relief ‘SBDR’ starts from 5,000hl to 2,100hl had in once sense been anticipated for a while due to the lobbying of the Small Brewers Duty Reform Coalition ‘SBDRC’ who sought amendment to current SBDR arrangements. To say that the news was met with anxiety and consternation by some of the smaller brewers in the sector (typically falling into the cohort under 5,000hl p.a), and who would broadly be recognised under the Society of Independent Brewers ‘SIBA’ would be no understatement.

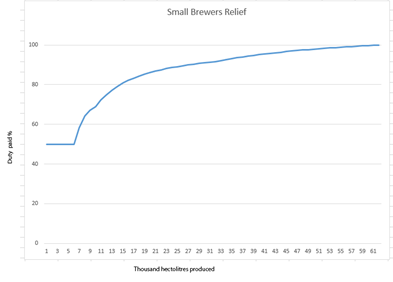

The graph below shows the current so called ‘cliff edge’ of Duty relief clawback (which starts at 50% and recedes to 0% duty relief at 60,000hl) that awaits brewers moving beyond the 5,000hl p.a. threshold, a task that has led many to effectively place a ceiling on their ambitions limited to the duty relief threshold level

Source: BeerNouveau.co.uk

The counterpoint has been that for many there has been no great incentive to breach the 5,000hl threshold, despite there having been an acknowledged need for overall change and better smoothing of the cliff edge to what is felt to be a more attainable level – ultimately the duty/tax take from HMRC also needs factored in (the latest proposal is mooted to be neutral to HMRC, but no further detail provided as of yet).

A sentiment, although not one you will find someone pinning their name directly to, was that the current regime meant that larger breweries saw the SBDR allow such a significant discount that it unfairly (in their eyes) opened up access to the pub fonts of smaller local brewers, who would otherwise not been able to compete with other stronger operators.

The beneficiary of the changes are likely to be the medium sized regional breweries already somewhere between 5,000hl and 60,000hl or indeed well beyond that point and who wish to see the relief extend up to 200,000hl, with the smaller players, who tend to not supply outwith a 30 mile localised radius, likely to feel the greatest impact of these changes.

Covid-19 impacts on the brewery sector

The immediate and most blunt impact of Covid 19 lockdowns were the near overnight shutting down of the ‘on trade’ market across all brewers. A common complaint, even before the impact of the proposed Duty changes were aired, was that depending on which part of the UK you were based, your brewery would have missed out on Covid 19 Grant payments of £25,000 (where retail and bars benefitted), and they will also have not been eligible for a waiver of business rates. It is also likely that your brewery will have been exempted from business interruption insurance and, in time as lockdown transition measures were introduced, you may not be seeing any direct benefits from measures such as the 5% VAT being related to food (alcohol also excluded from the Eat Out to Help Out scheme).

In the Scottish market there is also the added factor of the 2022 introduction of the Deposit Return Scheme which will charge a returnable deposit per single use container (bottle or can) on each unit sold, potentially also impacting the perception of added cost to end customers as well.

One could therefore wholly understand a slumping of the shoulders when the news of the Duty change then dropped last week…

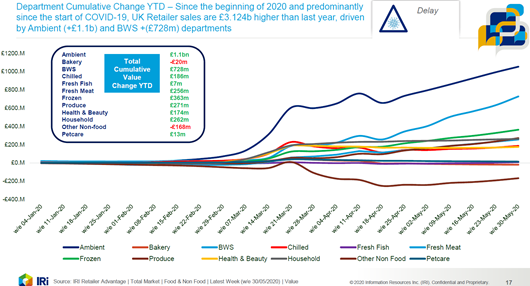

There are however, as ever, some positive signs if you chose to look closely during this period. For example, research for IRi below to end May 20 shows that beyond Ambient, Beer Wines & Spirits ‘BWS’ performed best year to date 2020 in retailer sales versus prior years

Whilst a positive move, and partial mitigation for bar closures, typically <5,000hl brewers don’t (or at best struggle to wrestle with pricing on) supply to major retailers, and a clear trend which has been observed within lockdown has been the shift from many of the smaller craft brewers towards a Direct to Consumer pathway.

This trend also has knock on implications for wholesalers, who may have spent a period of time in lockdown seeing the on-trade volume, to which they are reliant on to derive income, stalled. In the meantime, the ‘at home drinker’ has either been purchasing from their supermarket retailer, from an online aggregator or if wishing to support their preferred small brewery, buying cans or small pack directly from them. As lockdown eased, certain bars also opened up for ‘takeaway sales’ allowing some of the keg stocks that were left on the shelf back in March to be sold and to restart production for smaller brewers.

Whilst direct supply has a clear margin benefit for brewers, the picking and packing, as well as fulfilment requirements to cover modern e-commerce needs are a new and different skillset for some to accommodate, added to which come issues such as viability of minimum pack sizes to as well as requirements around stock holdings which also present their own challenges.

Where matters stand now – some unscientific market sentiment

As part of the process of writing this note we spoke to a variety of clients and contacts within the Brewing and related sectors to get a sense of their outlook in mid summer 2020 in light of these impacts. We sought responses on topics such as the direct and indirect impacts of the proposed SBDR changes, asked what feedback respondents would give towards the proposed ‘Technical consultation’ process, as well as commentary on direct to consumer supply, and trends that can be foreseen in the next 12 months if it is assumed that the proposed changes get ratified in due course.

Key themes of the feedback we received, but the main themes we derived were as follows:

- • The devil will be in the detail in terms of exact impact. What can be noted is that views on the proposed changes were markedly divided between those who were already embarked upon the ascent of or beyond the relief ‘cliff edge’ and those who were content to remain at a lower level of production and operation;

- • Keener eyes have also picked up on the proposal to change the duty to a fixed financial amount as opposed to a %, which could also be a means of reducing the relief as a whole versus inflationary effects;

- • The proposed changes are felt likely to push a ‘point of change’ decision onto brewers who are at or anticipating falling into the volume band of 2,000 – 5,000hl, where the option to just stay put, as you are, feels difficult;

- • The noted risk to around 150 breweries who would loose maximum relief feels inconsistent with the intention that “no brewery should loose out” with the proposed changes;

- • The smallest brewers also proportionally employ a greater staff per hectolitre produced, and so will therefore have potentially the largest staffing impacts;

- • Whatever happens with the detail on tapering of the relief, direct to consumer is a clear trend (surpassing on trade from 2017) and exacerbated further by the Covid crisis, with smarter centralised and collaborative fulfilment likely to be a key trend as this shift continues;

- • A consequence may be failure for some brewers, a need for consolidation and realisation of efforts to date for others that can sell, or for the more ambitious to answer the call this prompts to seek to grow and potentially create new craft brewing models to address the new market position; and

- • A review of social media posts to compare sentiment with the above shows a concerted effort from smaller brewers and industry commentators to influence governmental review (e.g. letter templates to send to MP’s) and the recognition from now larger brewers such as James Watt at Brewdog, where he noted that “SBDR was essential in their own early years of growth….the reduction of SBDR is a hammer blow to thousands of small brewers when they need it least”.

Sentiment towards Craft Beer and its impact on M&A and funding

The more sceptical end of observers of the Beer, Wines and Spirits sector have held the belief that the Craft Beer market, which has seen numerous notable acquisitions from larger mainstream operators in the past, as a ‘trend’ which will ultimately pass much like other fashions in the sector.

The model of building a brewery ‘brand’ to the 5,000hl threshold and then seeking a ‘big brother’ relationship or ownership to propel you up and beyond the duty escalator has certainly more recently become a more difficult sale than was perhaps hitherto the case. Consolidators within this space are more scarce (some notable high value acquisitions having failed to really hit the spot with some onward sales at a heavy loss in the US), and will likely prove more demanding in their requirements of target businesses, whether that be identifiable and leverageable brand and beers or on simple financial metrics.

Mainstream investor appetite within the sector is likely be focussed on those parties that have reached a certain level of scale and market penetration as they present a lower initial investment risk. In the context of relative industry scale, this could see smaller regional players take on board investor support, and to then enable and target further growth and addition of complimentary brands and smaller breweries mastheads. Gaps within existing portfolios and geographic expansion may be drivers of these initiatives.

A bold and alternative business growth thesis, which could yield a higher return to investment might also be to use the current circumstances and seek to build a model where the better branded and ambitious local breweries build a series of geographic clusters in key urban areas where Craft Beer has a stronger foothold (maintaining their 30 mile radius recognition and brand strength), under a shared ownership (potentially with investor support).

This type of approach may even tilt further towards a ‘collective/co-operative’ approach (moving beyond just making a beer together), where the focus on coming together could be towards areas such as enhanced buying power in procurement of malt and other supplies, sharing of certain key back office functions and on the market facing side, combining to lighten the load on e-commerce, D2C fulfilment and distribution, and extending market penetration and spread to fellow collective group members.

Any growth plan is of course easier to suggest than to implement, but the opportunity potentially exists for a consumer research driven approach, identification of the brands best placed in the eyes of consumers for growth. Models which apply data driven research and lower risks will be best placed to succeed in securing support to grow.

Conclusion – What Next then?

There are a number of potential reactions to the proposed changes, and with a likely implementation date of 2022 for the SBDR there is also a bit of time to observe and reflect on matters.

Reform is not yet quantified, nor adoption cut and dried – There has been a concerted effort from smaller brewers to push back on the proposals. Firstly, it is important to recognise that the announcement on 21st July was merely an initial conclusion. It is estimated by SIBA that around 150 breweries in the UK will be impacted by the proposed changes, seeing their duty levels rise.

Immediate market difficulties are likely to remain priorities, but opportunities will arise – With On trade anticipated for the meantime to be running at as low as c.15-25% of previous volumes depending on lockdown release, it would be a bold move to dare to predict the timeline and path of return and therefore embark now on a distinct growth strategy in that context. There is likely therefore to be a period of observation and consideration on plans across the board, though inevitably there will also be parties that have a clear path ahead and who seize the undoubted chances that the current flux presents.

D2C a growing focus – whilst D2C has offered a positive aspect to many in lockdown, the wider online delivery sector has itself started to attract watchful glances by the treasury, and therefore may be about to encounter its own challenges in taxation. There are a number of notable beer to consumer platforms who may see the current market position as a further opportunity and who are clearly keen to support the smaller brewers who lack their reach and capabilities, if they can fit within their model, with their key ongoing challenge being to give the consumer what they want within pricing and convenience levels. Anyone without a direct to consumer strategy either quickly needs to develop one or accept that they are losing a key foothold into the future market.

Moving collaboration beyond the brewing process – beer product collaborations are a well recognised and familiar theme, however given the wider trends noted above, there may perhaps become a more focus towards attention toward more operational collaboration – for instance in areas such as supply procurement, back office and admin functions, distribution/fulfilment routes, and bar install etc. may all need to be considered to allow competitive positioning versus better financed competitors.

The role of the Industry Umbrella body – the mix of factors at play might also prompt a move for umbrella bodies to more boldly shift from being seen as lobby routes for membership towards a more involved and active commercial and shared support structure for their membership.

Acquisition and investment plans – this will, as ever, be slightly in the eye of the beholder, and dependent on any perceived gaps in their ‘where to play’ strategy. Near all observers expect consolidation to happen, and indeed HMRC envisage providing some merger support mechanisms within the reform agenda.

So in summary, it feels like we are entering a time of some close monitoring of status, keeping a watchful eye on a number of competing factors (some very much outwith all of our control). It has always been the case, but perhaps more than ever for participants in the brewing sector right now, the option to stand still and hold your position whilst all of the above takes place is probably not an option anymore.

Harry Linklater

Director

harry@hnhgroup.co.uk