“With increasing concerns around climate change and the cost of energy, it’s no surprise to see growing appetite for investments in the renewable energy sector.”

Following the successive recent completions of the debt funded MBO of Realise Energy Services Ltd[i], and the investment into The Electric Storage Company[ii], HNH’s Head of Sustainability, Paul Gleghorne gives his thoughts on transactional activity for companies operating within the renewable energy sector.

“We have had an incredibly busy M&A market generally for

12-18 months, with a multitude of transactions across a range of sectors. The

rhetoric from institutional investors remains positive around the availability

of capital and their desire to deploy through all cycles. M&A activity and

investments will continue but with a combination of cost inflation, supply chain

issues, geopolitical uncertainty, and the remnants of COVID-19, we expect deals

to be more strategic and measured, where strong management teams and deal

structuring are likely to be key factors. Opportunities within defensive

industries, especially where regulation is driving investment, will remain

attractive.”

Paul explains that appetite for opportunities in the

renewable energy sector has remained particularly high.

“The steep rise in the cost of energy has highlighted the overreliance

on conventional energy generation. Many large energy users are now seeking to

lower their marginal cost of energy use by installing solar panels and

batteries or even opting to build their own renewable energy generation as

private wire projects. In addition, it is becoming increasingly important for

companies to demonstrate their green credentials to customers with ESG

reporting requirements. On the other side, whilst financial returns ultimately

drive decision making, investors are becoming increasingly eager to provide funding

or invest in opportunities which assist in achieving their ESG targets.”

“It’s not all asset-based investments either, there are a

host of companies providing services that facilitate the use of renewable

energy. The recent deals of Realise Energy Services, who operate and maintain over

200 wind turbines across the UK, and power engineering and technology business The

Electric Storage Company, attracted considerable interest with some interested

parties citing green credentials as a contributing factor in their decision

making.”

HNH Corporate Finance have a dedicated team with a specific

focus on transactions in the sustainability sectors, ranging from sell/buy side

M&A, raising project finance and appraising investment opportunities.

[i] The

MBO of Realise Energy Services Ltd was funded by specialist credit provider

Beach Point Capital

HNH are

delighted to welcome Lucas Batchelor as an Assistant Manager to our Deal

Advisory team.

Lucas graduated

from Queen’s University Belfast with first class honours, completing a BSc in

Economics with Finance. During his time at the university, he was awarded the

prestigious Porter Scholarship. Lucas completed his training as a chartered

accountant in KPMG’s audit team in Belfast. He is currently completing an MSc

in Data Analytics at the University of Glasgow and has recently submitted his

final dissertation, “Comparing the performance of bankruptcy prediction

methods”.

His appointment

illustrates the continuing expansion and development of the Deal Advisory team.

“Paul Gleghorne commented: “We are delighted to further bolster our team

within the Corporate Finance and Financial Modelling service lines. Whilst

2022/2023 will have more complexities for those considering embarking on

M&A, we have an exciting pipeline of work and this is a sign of continued

investment in our growing team.”

Lucas said, “I

am thrilled to begin my new role within the Deal Advisory team at HNH. I am

looking forward to working with a wide variety of quality clients and

continuing my professional development within a team of high calibre

individuals.”

HNH acted as Lead Corporate Finance Advisor for Powerhouse. HNH

Head of Sustainability, Paul Gleghorne, commented “HNH were delighted to act

for the company on this transaction. Powerhouse provides vital services to

facilitate renewable energy on the grid and reduce energy demands of large

consumers. The acquisition by Cool Planet Group will facilitate the growth of

the company’s services in the sector.”

Powerhouse Generation Ltd was founded in 2013 as a DSU

aggregator operating within Ireland’s electricity market. Since inception,

Powerhouse has added DS3 trading and consultancy services to its offering.

Powerhouse Energy Management Ltd was setup in 2019 and acts as an advisor and

broker in the energy sector giving Powerhouse a full suite of energy management

services.

HNH Head of Deal Advisory, Richard Moorehead, stated “this

transaction is indicative of HNH’s increased focus on working with companies in

the sustainability sectors, including renewable energy and waste management.

These sectors are key growth areas for HNH and we are continuing to grow our Sustainability

team in Belfast.”

Commenting on the acquisition, Richard Watson, Chairman of

Powerhouse, said “we are looking forward to working with Cool Planet Group and accelerating

our growth plans and expansion into new markets.”

Alan Keogh, chief executive of Crowley Carbon, says Powerhouse’s

“demand response capabilities will compliment our existing offerings of solar

PV, battery storage, electrification of heat, EV chargers and vehicle to grid,

enabling us to reduce carbon and greenhouse gas emissions in plants for a net

zero future. We can now create new offerings that combine energy efficiency,

renewable power, EV-charging and sustainability and compliance reporting to

help organisations reach their net-zero carbon goals.”

Tughans in Belfast, led by James Donnelly, acted as legal

advisors to Powerhouse.

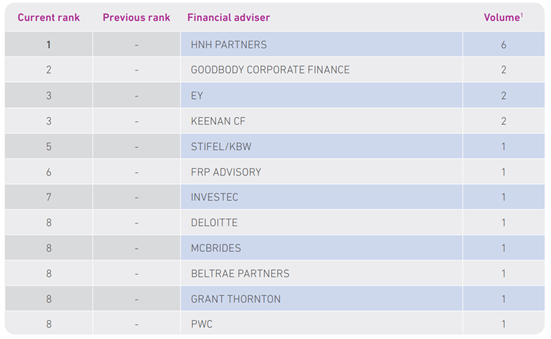

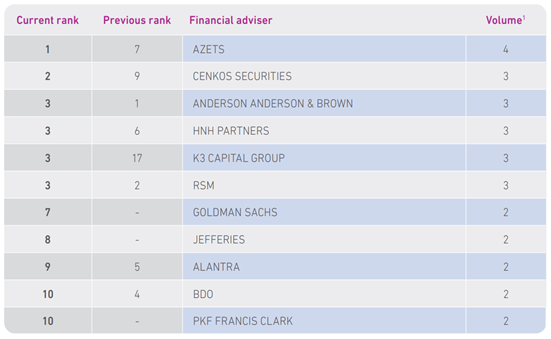

With the publication of the latest Experian M&A League Tables, we are very pleased to report that our Deal Advisory team in Northern Ireland has maintained its position as the leading corporate finance advisor in the region, closing nine deals in the first half of the year.

Our Scottish team continued its strong start to the year, closing seven transactions throughout H1.

We are delighted to see the efforts of our deal advisory teams in NI and Scotland recognised by their strong showings in the Experian UK & RoI M&A League Tables for Q1 2021. Our NI team was the most active in the country, completing six transactions in the quarter, while our Scottish team narrowly missed out on top spot, closing three deals in the period.

The Deal Advisory team at HNH is delighted to announce two pieces of good news:

Chris Hylands joined the team in December 2018 and, over the past two and a bit years, has worked on a wide range of transactions across NI and Scotland. In recognition of his hard work and technical development, we are very pleased to announce his promotion to manager, effective 1 April.

On the other side of the Irish Sea, we welcome Craig McGill to the Edinburgh office. Craig joins us as an assistant manager and brings the team in Scotland to five. His appointment comes at a good time with activity levels building strongly this year and continuing the trend that we started to see in the final quarter of 2020.

A double helping of good news today as we announce two new additions to Deal Advisory and Transaction Services and congratulate two existing team members on their promotions.

Paul Gleghorne has been promoted to Associate Director in our Deal Advisory Team and will take the lead on engagements in the waste, energy and renewables sectors in addition to continuing his leadership role within financial modelling engagements. Peter Graham has been promoted to Senior Manager in our Deal Advisory team.

Duncan Thorburn joins our Deal Advisory team in Edinburgh as a Senior Manager from a similarly-positioned M&A boutique in Scotland, where he has been working across both corporate finance and TS for the last five years. He was previously at RBS, having joined their graduate scheme and fulfilled a number of customer facing and internal reporting roles.

Duncan arrives with strong experience and insight into the Scottish Tech sector and the wider SME funding environment, and we recently worked in conjunction with him when he undertook a buyer diligence role for Maven on Quorum Cyber, the MBO HNH advised on in June 2020.

Harry Linklater, Deal Advisory Director for Scotland, welcomed Duncan to the team, saying , “We believe that adding Duncan into the fold at HNH will be a key strategic addition to our team in Scotland, bolstering the ability we offer to provide experienced and relevant input to the technology and wider market here at HNH. Our focus has always centred on delivering best in class advice at a senior level, with an emphasis on local clients and Duncan’s addition enhances that’.

Duncan added, “I am excited to take up my new role with HNH and look forward to continuing to build on relationships I have developed with both clients and the investor market”

In 2018, we launched a Transaction Services division under the leadership of Rodney McCaughey. Since then, we have carried out FDD engagements for corporate acquirers, debt providers and private equity investors on transactions throughout the UK and Ireland. Highlights include the investment in the CRS by Renatus Capital Partners and the investment in Kingsbridge Healthcare Group by Foresight and 57 Stars.

On the back of the success of the last two years and with a strong pipeline of work, we are pleased to welcome Tom Swatman to our TS team as an Assistant Manager. Tom qualified as an accountant with Harbinson Mulholland in Belfast and prior to that gained experience working with Bank of America Merrill Lynch in London.

Congratulations to Paul and Peter on well-deserved promotions and a very warm welcome to Duncan and Tom.

Perhaps a new era and form of collaboration/consolidation?

An already precarious business outlook for many small breweries across the UK, who had just about boxed and weaved their way through the impact of Covid 19 were dealt a potentially fatal blow from the proposed change in the Small Brewers Duty regime in late July, with the added uncertainly of an increasingly likely ‘no deal’ Brexit also looming.

The news released on 21st July that the UK Government had decided to reduce the threshold at which Small Brewers Duty Relief ‘SBDR’ starts from 5,000hl to 2,100hl had in once sense been anticipated for a while due to the lobbying of the Small Brewers Duty Reform Coalition ‘SBDRC’ who sought amendment to current SBDR arrangements. To say that the news was met with anxiety and consternation by some of the smaller brewers in the sector (typically falling into the cohort under 5,000hl p.a), and who would broadly be recognised under the Society of Independent Brewers ‘SIBA’ would be no understatement.

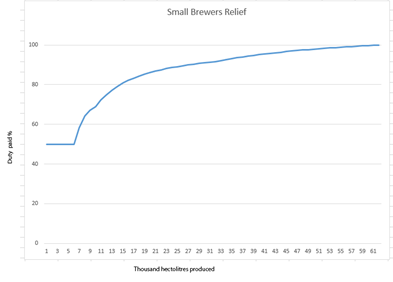

The graph below shows the current so called ‘cliff edge’ of Duty relief clawback (which starts at 50% and recedes to 0% duty relief at 60,000hl) that awaits brewers moving beyond the 5,000hl p.a. threshold, a task that has led many to effectively place a ceiling on their ambitions limited to the duty relief threshold level

Source: BeerNouveau.co.uk

The counterpoint has been that for many there has been no great incentive to breach the 5,000hl threshold, despite there having been an acknowledged need for overall change and better smoothing of the cliff edge to what is felt to be a more attainable level – ultimately the duty/tax take from HMRC also needs factored in (the latest proposal is mooted to be neutral to HMRC, but no further detail provided as of yet).

A sentiment, although not one you will find someone pinning their name directly to, was that the current regime meant that larger breweries saw the SBDR allow such a significant discount that it unfairly (in their eyes) opened up access to the pub fonts of smaller local brewers, who would otherwise not been able to compete with other stronger operators.

The beneficiary of the changes are likely to be the medium sized regional breweries already somewhere between 5,000hl and 60,000hl or indeed well beyond that point and who wish to see the relief extend up to 200,000hl, with the smaller players, who tend to not supply outwith a 30 mile localised radius, likely to feel the greatest impact of these changes.

Covid-19 impacts on the brewery sector

The immediate and most blunt impact of Covid 19 lockdowns were the near overnight shutting down of the ‘on trade’ market across all brewers. A common complaint, even before the impact of the proposed Duty changes were aired, was that depending on which part of the UK you were based, your brewery would have missed out on Covid 19 Grant payments of £25,000 (where retail and bars benefitted), and they will also have not been eligible for a waiver of business rates. It is also likely that your brewery will have been exempted from business interruption insurance and, in time as lockdown transition measures were introduced, you may not be seeing any direct benefits from measures such as the 5% VAT being related to food (alcohol also excluded from the Eat Out to Help Out scheme).

In the Scottish market there is also the added factor of the 2022 introduction of the Deposit Return Scheme which will charge a returnable deposit per single use container (bottle or can) on each unit sold, potentially also impacting the perception of added cost to end customers as well.

One could therefore wholly understand a slumping of the shoulders when the news of the Duty change then dropped last week…

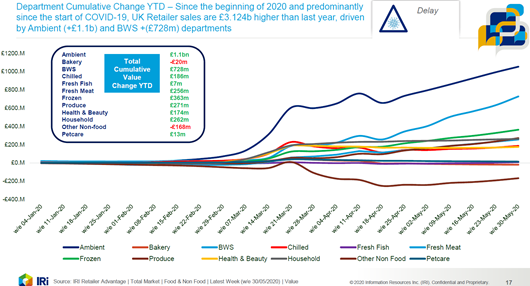

There are however, as ever, some positive signs if you chose to look closely during this period. For example, research for IRi below to end May 20 shows that beyond Ambient, Beer Wines & Spirits ‘BWS’ performed best year to date 2020 in retailer sales versus prior years

Whilst a positive move, and partial mitigation for bar closures, typically <5,000hl brewers don’t (or at best struggle to wrestle with pricing on) supply to major retailers, and a clear trend which has been observed within lockdown has been the shift from many of the smaller craft brewers towards a Direct to Consumer pathway.

This trend also has knock on implications for wholesalers, who may have spent a period of time in lockdown seeing the on-trade volume, to which they are reliant on to derive income, stalled. In the meantime, the ‘at home drinker’ has either been purchasing from their supermarket retailer, from an online aggregator or if wishing to support their preferred small brewery, buying cans or small pack directly from them. As lockdown eased, certain bars also opened up for ‘takeaway sales’ allowing some of the keg stocks that were left on the shelf back in March to be sold and to restart production for smaller brewers.

Whilst direct supply has a clear margin benefit for brewers, the picking and packing, as well as fulfilment requirements to cover modern e-commerce needs are a new and different skillset for some to accommodate, added to which come issues such as viability of minimum pack sizes to as well as requirements around stock holdings which also present their own challenges.

Where matters stand now – some unscientific market sentiment

As part of the process of writing this note we spoke to a variety of clients and contacts within the Brewing and related sectors to get a sense of their outlook in mid summer 2020 in light of these impacts. We sought responses on topics such as the direct and indirect impacts of the proposed SBDR changes, asked what feedback respondents would give towards the proposed ‘Technical consultation’ process, as well as commentary on direct to consumer supply, and trends that can be foreseen in the next 12 months if it is assumed that the proposed changes get ratified in due course.

Key themes of the feedback we received, but the main themes we derived were as follows:

• The devil will be in the detail in terms of exact impact. What can be noted is that views on the proposed changes were markedly divided between those who were already embarked upon the ascent of or beyond the relief ‘cliff edge’ and those who were content to remain at a lower level of production and operation;

• Keener eyes have also picked up on the proposal to change the duty to a fixed financial amount as opposed to a %, which could also be a means of reducing the relief as a whole versus inflationary effects;

• The proposed changes are felt likely to push a ‘point of change’ decision onto brewers who are at or anticipating falling into the volume band of 2,000 – 5,000hl, where the option to just stay put, as you are, feels difficult;

• The noted risk to around 150 breweries who would loose maximum relief feels inconsistent with the intention that “no brewery should loose out” with the proposed changes;

• The smallest brewers also proportionally employ a greater staff per hectolitre produced, and so will therefore have potentially the largest staffing impacts;

• Whatever happens with the detail on tapering of the relief, direct to consumer is a clear trend (surpassing on trade from 2017) and exacerbated further by the Covid crisis, with smarter centralised and collaborative fulfilment likely to be a key trend as this shift continues;

• A consequence may be failure for some brewers, a need for consolidation and realisation of efforts to date for others that can sell, or for the more ambitious to answer the call this prompts to seek to grow and potentially create new craft brewing models to address the new market position; and

• A review of social media posts to compare sentiment with the above shows a concerted effort from smaller brewers and industry commentators to influence governmental review (e.g. letter templates to send to MP’s) and the recognition from now larger brewers such as James Watt at Brewdog, where he noted that “SBDR was essential in their own early years of growth….the reduction of SBDR is a hammer blow to thousands of small brewers when they need it least”.

Sentiment towards Craft Beer and its impact on M&A and funding

The more sceptical end of observers of the Beer, Wines and Spirits sector have held the belief that the Craft Beer market, which has seen numerous notable acquisitions from larger mainstream operators in the past, as a ‘trend’ which will ultimately pass much like other fashions in the sector.

The model of building a brewery ‘brand’ to the 5,000hl threshold and then seeking a ‘big brother’ relationship or ownership to propel you up and beyond the duty escalator has certainly more recently become a more difficult sale than was perhaps hitherto the case. Consolidators within this space are more scarce (some notable high value acquisitions having failed to really hit the spot with some onward sales at a heavy loss in the US), and will likely prove more demanding in their requirements of target businesses, whether that be identifiable and leverageable brand and beers or on simple financial metrics.

Mainstream investor appetite within the sector is likely be focussed on those parties that have reached a certain level of scale and market penetration as they present a lower initial investment risk. In the context of relative industry scale, this could see smaller regional players take on board investor support, and to then enable and target further growth and addition of complimentary brands and smaller breweries mastheads. Gaps within existing portfolios and geographic expansion may be drivers of these initiatives.

A bold and alternative business growth thesis, which could yield a higher return to investment might also be to use the current circumstances and seek to build a model where the better branded and ambitious local breweries build a series of geographic clusters in key urban areas where Craft Beer has a stronger foothold (maintaining their 30 mile radius recognition and brand strength), under a shared ownership (potentially with investor support).

This type of approach may even tilt further towards a ‘collective/co-operative’ approach (moving beyond just making a beer together), where the focus on coming together could be towards areas such as enhanced buying power in procurement of malt and other supplies, sharing of certain key back office functions and on the market facing side, combining to lighten the load on e-commerce, D2C fulfilment and distribution, and extending market penetration and spread to fellow collective group members.

Any growth plan is of course easier to suggest than to implement, but the opportunity potentially exists for a consumer research driven approach, identification of the brands best placed in the eyes of consumers for growth. Models which apply data driven research and lower risks will be best placed to succeed in securing support to grow.

Conclusion – What Next then?

There are a number of potential reactions to the proposed changes, and with a likely implementation date of 2022 for the SBDR there is also a bit of time to observe and reflect on matters.

Reform is not yet quantified, nor adoption cut and dried – There has been a concerted effort from smaller brewers to push back on the proposals. Firstly, it is important to recognise that the announcement on 21st July was merely an initial conclusion. It is estimated by SIBA that around 150 breweries in the UK will be impacted by the proposed changes, seeing their duty levels rise.

Immediate market difficulties are likely to remain priorities, but opportunities will arise – With On trade anticipated for the meantime to be running at as low as c.15-25% of previous volumes depending on lockdown release, it would be a bold move to dare to predict the timeline and path of return and therefore embark now on a distinct growth strategy in that context. There is likely therefore to be a period of observation and consideration on plans across the board, though inevitably there will also be parties that have a clear path ahead and who seize the undoubted chances that the current flux presents.

D2C a growing focus – whilst D2C has offered a positive aspect to many in lockdown, the wider online delivery sector has itself started to attract watchful glances by the treasury, and therefore may be about to encounter its own challenges in taxation. There are a number of notable beer to consumer platforms who may see the current market position as a further opportunity and who are clearly keen to support the smaller brewers who lack their reach and capabilities, if they can fit within their model, with their key ongoing challenge being to give the consumer what they want within pricing and convenience levels. Anyone without a direct to consumer strategy either quickly needs to develop one or accept that they are losing a key foothold into the future market.

Moving collaboration beyond the brewing process – beer product collaborations are a well recognised and familiar theme, however given the wider trends noted above, there may perhaps become a more focus towards attention toward more operational collaboration – for instance in areas such as supply procurement, back office and admin functions, distribution/fulfilment routes, and bar install etc. may all need to be considered to allow competitive positioning versus better financed competitors.

The role of the Industry Umbrella body – the mix of factors at play might also prompt a move for umbrella bodies to more boldly shift from being seen as lobby routes for membership towards a more involved and active commercial and shared support structure for their membership.

Acquisition and investment plans – this will, as ever, be slightly in the eye of the beholder, and dependent on any perceived gaps in their ‘where to play’ strategy. Near all observers expect consolidation to happen, and indeed HMRC envisage providing some merger support mechanisms within the reform agenda.

So in summary, it feels like we are entering a time of some close monitoring of status, keeping a watchful eye on a number of competing factors (some very much outwith all of our control). It has always been the case, but perhaps more than ever for participants in the brewing sector right now, the option to stand still and hold your position whilst all of the above takes place is probably not an option anymore.

HNH’s Scottish team uses its expertise to support Edinburgh cyber security company

Despite challenging economic conditions, boutique corporate finance specialists HNH have helped Quorum Cyber Security Limited secure growth capital investment to scale its business internationally.

Led by HNH director Neal Allen, the Scottish arm of the Belfast-based multi-disciplinary financial advisory firm secured the £2.7m investment from Maven Capital Partners through its VCTs, alongside the Scottish Investment Bank, which will allow the Edinburgh-headquartered cyber security and data confidence services company to scale up.

In a sign of the resilience of the Scottish tech sector and the appetite for investment in ambitious Scottish businesses, the growth capital deal was instigated by Quorum Cyber’s managing director Federico Charosky, who has a 40% stake in the business.

With

a turnover of £2.7m and a team of 25 operating from Edinburgh, Quorum Cyber

provides a professional and managed security services for UK and international

clients including a fully managed detect and response capability via the

company’s Microsoft Azure Sentinel Security Operations Centre (SOC). Charosky

will use the growth capital to further scale the business, investing in sales

and marketing resource, as well as product innovation to ensure clients can

confidentially operate within an increasingly hostile cybersecurity

environment.

Allen

and the HNH team, which specialises in advising SMEs and entrepreneurs on

M&A and growth capital activity, spent several months working with Quorum

Cyber to secure the most appropriate investment solution. Having identified

several potential investors among its extensive network, HNH secured the

investment from Maven Capital, one of the UK’s most active private equity houses.

Allen,

director – deal advisory at HNH, said: “While Covid-19 and Brexit have created

a challenging financial climate, this growth capital investment demonstrates

that there is appetite for growth and investment in Scottish business. It was very encouraging that there was a lot of interest

among Scottish based private equity/venture capital funds and we’re

delighted to have facilitated this for Quorum Cyber. The team at Maven Capital

Partners led by David Millroy were very receptive from the start and we know

that Maven is the right home for this business as it continues to grow its

client base around the world.”

Charosky

said: “Working with HNH and Maven to create the deal has been a fantastic

experience. This deal will enable Quorum Cyber to continue growing in a

sustainable way, ensuring we continue to exceed customer expectations, while

protecting the amazing culture we’ve created.”

Millroy,

a partner at Maven Capital Partners, said: “We are delighted to be leading the

investment in Quorum Cyber and look forward to being part of its growth in the

years to come. The senior team have

already created a strong business and there is significant opportunity to scale

operations globally, with further expansion already underway in the Middle

East, Australia, South Korea, and North America.”

The Edinburgh office of HNH opened in April 2019. In March this year, HNH’s Edinburgh team secured a £30 million asset-based lending package for The GlenAllachie Distillers Co from Clydesdale Bank. Other clients have been drawn from food and drink, manufacturing, building products, business services and transport sectors.

Deal Advisory director Neal Allen recently gave a presentation to ICAEW members in Scotland on the implications of COVID-19 on the outlook for fundraising and M&A activity. A copy of the presentation is available to download via the following link

The past months have had a deep

and lasting impact for all of us. In February, the terms social distancing,

furloughing and COVID-19 were almost unheard of and now they are part of our

everyday ‘virtual’ lexicon. The world has tilted on its axis and life for all

of us has changed. Indeed for many the enforced extra down time will have

provided an opportunity for some strategic thinking and planning for the future;

entrepreneurs and business owners may well have turned their thoughts to the

possibility of selling up, cashing in or moving in a different direction. For

those who are contemplating such a move (even if they don’t want to admit it!)

the next question is how might they go about it?

When a decision has been made to

sell/exit a company, one needs to consider the options, select the most

suitable one, prepare a comprehensive plan and implement the plan accordingly.

While most business owners will recognise this process as being part of their everyday

business makeup, when it comes to actually selling your company/business, the

big difference is that most people only do this once or by exception a couple

of times in their lifetime and thus it is not a process that they are entirely

familiar with. So what are the key

factors to consider?

If the decision has been taken to sell, then the first key factor is to work out who is going to buy the business. In an article last year we discussed the various exit routes that are typically open to shareholders. For many businesses, taking them to market via a trade sale process is the preferred option, in that, more often than not, it results in the highest valuation being achieved.

However, as we embark on what

will likely be a lengthy recovery period post-COVID, it may be that for some

businesses a trade sale is no longer the best direction. Prospective buyers may

be preoccupied with their own internal issues, or may approach M&A activity

with an opportunistic mindset unlikely to lead to an acceptable valuation for

the seller.

In these circumstances, it is

therefore more important than ever to weigh up the alternative options. Four that

we will examine in more detail are: the Management Buy-out; the Management Buy-in;

the Employee Buy-out and the Members Voluntary Liquidation.

The Management Buy-Out (MBO)

In its simplest form an MBO, is a

deal in which members of the company’s incumbent management team acquire all of

or a controlling stake in the business from the existing shareholders.

Typically, this involves the creation of a new company (Newco), which is used to

acquire the shares (or in some cases the trade and assets) of the trading

company.

Typically, the MBO team will not

have access to sufficient personal resources to complete the deal with a full

cash consideration. Depending on the nature of the business, the long-term

growth strategy and how much the team can commit personally, it may be possible

to bridge the gap by bringing in external funders such as a PE fund, debt fund,

or bank. Equally, it may be possible for the vendor(s) to part-finance the deal

via deferral of a proportion of the consideration or via loan notes in Newco.

There are quite a few tax

considerations in an MBO, not only for the existing owner but also for the

management team and the buyout company. The vendors will want to ensure that

they qualify for capital gains tax treatment in respect of the proceeds they

receive and also maximise their entitlement to Business Asset Disposal Relief

(‘BADR’, previously known as Entrepreneurs’ Relief). This is now only available

for gains of up to £1m but still saves £100,000 in tax per qualifying

shareholder. If they are going to retain a minority interest in the company or

help finance it via loan notes then the share for share/loan note exchange

rules can come into play and a pre-transaction clearance from HMRC is strongly

advised to ensure that the anti-avoidance rules will not be applied so as to

treat the transaction as being subject to income tax. On top of this there may

be a need to elect to dis-apply the share for share/loan note rules in certain

circumstances if this could lead to a loss of entitlement to BADR. The MBO team will also need to be mindful of

the tax legislation that applies to employment related shares and they may also

need to consider making certain elections to avoid future exposure to income

tax arising on the ultimate sale of their shares in the buyout company. It

would therefore be important to have all of these matters considered and

planned for prior to completing the MBO.

The

Management Buy-In (MBI)

An MBI can be viewed as a hybrid

of an MBO and a trade sale in that an external team acquires the business from

the existing shareholders. To all intents and purposes the structure of an MBI

is the same as for an MBO: a Newco will be established as the acquisition vehicle,

it will raise the necessary finance to execute the deal and ultimately acquire

the business.

The funding options for an MBI

are the same as for an MBO in that the team will typically need to augment what

they can bring to the table with some third party funding. That said, it can be

more difficult to raise finance for an MBI as, by definition, it involves an

external team taking over the business and funders are often concerned that a

lack of familiarity with the business, or cultural clashes with staff can

increase the risk of post-completion setbacks.

The tax considerations for the

vendors will be similar to those noted above in respect of the management

buyout in that the sellers will want to ensure that they qualify for capital

gains tax treatment in respect of the proceeds they receive and also maximise

their entitlement to BADR. Once again, if they are going to retain a minority

interest in the company or help finance it via loan notes then a pre-transaction

clearance from HMRC is strongly advised in respect of any share for share/loan

note exchange. Also the vendors may wish to elect to dis-apply the share for

share/loan note rules in certain circumstances if this could lead to a loss of

entitlement to BADR. As the MBI team (which

may include some of the existing management) will become employees, they will need

to take account of the employment related share rules, which may entail making an

election to avoid future exposure to income tax arising on the ultimate sale of

their shares in the company. Once again some pre-transaction tax planning is

highly recommended.

Employee Buy-Out (EBO)

An option that is growing in popularity, but still somewhat under the

radar, is the EBO. Under this option,

rather than a small group of managers acquiring the business (an MBO), the

entire workforce participates in the deal, either directly or indirectly. Indirect participation in the EBO is

generally via an employee ownership trust that acquires shares on behalf of the

beneficiaries.

While the EBO is a relatively uncommon option, there are some high

profile examples of employee-owned businesses, with John Lewis/Waitrose

probably the most well-known. With employee engagement an increasingly hot

topic and retiring shareholders keen to protect their legacies, an EBO can be

an exit route that is worth exploring.

From a tax perspective a sale of

the shares in a trading company (or trading group) by existing shareholders to

an employee ownership trust will be deemed for tax purposes to be for a

consideration that gives rise to neither a capital gain nor a capital loss – in

effect the transfer will be deemed to be tax free. There are several criteria

which need to be met including that the trust must be solely for the benefit of

all eligible employees of the company on the same terms. An eligible employee

excludes any current shareholder with a holding in excess of 5% (taking into

account holdings of anyone who is connected with the shareholder). After the

share transfer, the trust must control more than half of the shares, votes,

profits available for distribution and assets available on a winding up of the

company. There are several other criteria that must also be met for the

favourable tax treatment to apply in respect of disposals to an employee

ownership trust. It is therefore imperative that careful consideration is given

to the detailed rules in advance of shareholders disposing of their shares to

such a vehicle and being entitled to claim the capital gains tax relief. If the

requisite rules can’t be met then any disposal to such an employee trust should

be within the charge to capital gains tax, at a rate of 10% if the conditions

for BADR are met (and 20% on gains in excess of £1m or where the conditions for

BADR are not met).

Members’ Voluntary liquidation

Sometimes there may be little of the original business to carry on once the main shareholders decide to call it a day (especially if the service provided by the company is dependent on the shareholders’ skill sets). In such cases, where there has been a build-up of undistributed cash and assets, it is possible for the business to cease and the company to enter into a members’ voluntary (solvent) liquidation.

This is a formal insolvency

process in which a licensed insolvency practitioner is appointed to take control

of the company, liquidate all of its assets and, after paying off all creditors,

distribute the remaining assets and cash of the company to the shareholders and

then wind up the company. Whilst the process is formal and requires strict

compliance with the insolvency rules and company law, it is a well-trodden path

for experienced insolvency advisors who under the right circumstances can

distribute a significant majority of the company assets to the shareholders

shortly after they have been appointed, with the remainder of the assets being

distributed after the formal requirements of the liquidation process have all

been completed.

For tax purposes the main benefit

of a members voluntary liquidation is that the distributions should be treated

as capital distributions for tax purposes and thus subject to capital gains tax

treatment at a rate of 10% if the conditions for BADR are met (and 20% on gains

in excess of £1m or where the conditions for BADR are not met). This provides a

big advantage over normal income distributions/distributions which are subject

to income tax at up to 38.1%.

However, there is a nasty tax trap

that can arise for those who go down this route and then decide to start up

again in the same or similar business under a different vehicle within a two

year period following the liquidation of the original company. If a shareholder

either sets up a new company or even starts up

a similar business by himself/herself or in partnership with someone

else, HMRC may apply the ‘anti phoenixism’ rules which enables them to treat the liquidation distribution as being

subject to income tax and not capital

gains tax. Falling into this trap could result in an additional tax charge of

almost 30%. Once again careful planning and consideration is required.

So if you are thinking that it might be time to ‘cash in your chips’, there are various ways that you might be able to do so, even if a third party purchaser is not on the horizon.

For any of our clients or contacts who are unsure of what support packages are available to help them navigate these uncertain times, or how to avail of them, we have prepared a downloadable summary of the situation as it currently stands.

The GlenAllachie Distillers Co. Limited has secured a £30 million asset-based lending package from Clydesdale Bank, thanks to support from the new Scottish arm of Belfast-based finance specialists HNH.

The award-winning whisky company appointed Bruce Walker, director of HNH’s Edinburgh team, to lead the refinancing exercise. The Scottish office of HNH was established last year to advise SMEs and family-owned firms during mergers & acquisitions, debt and transaction services.

HNH advised GlenAllachie on securing an inventory only asset-based debt facility on a committed basis for a four-year period on significantly improved terms. Clydesdale Bank Plc was selected to provide the facility on a bilateral basis following a competitive tendering process, which was developed and manged by HNH.

GlenAllachie, winners of the Distillery of the Year Award at The Scottish Whisky Awards, will use the facility to fund working capital and capital expenditure as it continues to develop its brand around the world.

The GlenAllachie distillery, which is located near Aberlour in the heart of the world-renowned Speyside region, and a significant volume of mature whisky was bought from Chivas by Billy Walker and his team in 2017.

The business has quickly earned a reputation as a producer of premium single malt whisky. Its award-winning current products include GlenAllachie’s core range of aged single malts and the richly peated blended malt, MacNair’s Lum Reek. The White Heather brand is also owned by GlenAllachie, and will be relaunched in May of this year.

Billy Walker, the managing director of GlenAllachie, said: “This new debt facility will enable us to continue our journey at the pace we want and further develop GlenAllachie as a premium single malt brand around the world.”

Bruce Walker from HNH, added: “This deal is a great result for GlenAllachie, and the outcome of a competitive process led locally by the HNH team. We were delighted to work with such a high-quality asset with an outstanding management team with a crystal clear strategic vision. It was also good to work again with Clydesdale Bank Plc who were able to deliver a compelling proposal based on their clear understanding of the sector and strong existing relationship with the GlenAllachie team. Appetite for the credit was strong reflecting the strength of both the business and the whisky market more widely.”

Alan Gilchrist, the finance director of GlenAllachie, said: “HNH’s clear understanding of the debt markets, ABL product and current lender appetite was key in securing our new facilities in the required timeframe. We were very pleased with the way Bruce and Fiona King of HNH managed the process and left us to continue running the business. The input we received from HNH was invaluable in securing our deal. Asset-based lending is ideal for us as it provides highly flexible funds secured against our appreciating whisky stocks.

“Clydesdale Bank Plc demonstrated an assured and mature approach to the deal process. They maintained momentum to ensure delivery to timetable and a deep knowledge of the Scotch whisky sector to create a straightforward solution from a clear requirement.”

David Hunter, director, asset based lending with Clydesdale Bank Plc, Glasgow, commented: “We are looking forward to working with the management team at GlenAllachie and are delighted to be able support them through such an exciting stage of their business.”

Three senior professionals from Scotland’s leading accountancy practices have come together to help drive HNH’s expansion into the GB market. The new office will provide SMEs with access to some of Scotland’s most senior corporate finance professionals, offering tier one advice and experience, but tailored to the needs of smaller and family-owned firms.

Based in Edinburgh’s Charlotte Square, the new team consists of Neal Allen, Harry Linklater and Bruce Walker. Prior to joining HNH, Neal was head of M&A for KPMG Scotland, Harry was a partner in French Duncan LLP and Bruce led KPMG Scotland’s debt advisory team.

The new team, which will initially focus on providing M&A, debt and transaction services, has already completed an advisory role for foodservice firm R&W Scott as well as a significant funding role in the distilling sector. Other clients have been drawn from financial services, manufacturing, building products and transport sectors.

Director Neal Allen said: “We’re all excited to join HNH and build the business in Scotland by offering SMEs a new approach to corporate advice. While some business owners are rightly cautious because of Brexit and global economic concerns, many of our contacts, particularly in food services, are telling us they want to execute growth plans. By providing senior-level advice, which was previously viewed as the preserve of larger firms, we can help SMEs grow through potential headwinds by securing the right funding options, partners and acquisition targets.”

Harry Linklater, Director. added: “Having developed client relationships over time with a focus on the Scottish SME sector, I’m keen to continue working with long-established contacts within a progressive advisory focused firm. As we build our presence in Scotland as HNH, we will leverage the firm’s relationships with equity and debt funders across various locations, to offer the Scottish market something new and different.”

Bruce Walker, who joins as a director at HNH after 25 years with KPMG, said: “The boutique business model at HNH allows us to react to clients’ requirements quickly and to adapt accordingly. The entrepreneurial nature of the firm, investing in growth and expanding into new markets will, we believe, give us a natural affinity with the SMEs which make up a major part of the Scottish economy. Over the past eight years, HNH has built a strong reputation as a leading corporate finance practice in Northern Ireland. We are excited about building upon that in Scotland, where the mix of SME advisory opportunities fits well with the team’s past experience and outlook.”

HNH is a well-established, independent Northern Ireland-based company which works extensively with the directors and shareholders of entrepreneurial companies throughout the UK and Ireland. The company was ranked at the top of Experian’s H1 Deal Activity Report, both in terms of deals completed and deal value in Northern Ireland.

Scottish clients will have access to its expertise in corporate finance, transaction services, business restructuring, taxation, forensic accounting and human capital. The new office represents a significant investment by the firm in establishing its first office outside Northern Ireland.

HNH recently advised Belfast-based IT support business CMI in its acquisition of London-based IT firm BTA. Funded by Panoramic Growth Equity in Glasgow the deal takes CMI’s turnover to in excess of £11m. HNH expects the new Scottish office will help identify opportunities for more deals spanning the Irish Sea.

Craig Holmes, Managing Director of HNH, said: “This is an exciting move for HNH as we build on great foundations in Northern Ireland to extend our offering to Scotland. Assembling a team as strong as this demonstrates how confident we are in the Scottish economy. While initially focusing on M&A, HNH in Scotland will also have access to our business restructuring, tax advisory, forensic and human capital teams.

“The opportunity to hire three of the best networked corporate advisors in Scotland, with unsurpassed market knowledge and deal experience, and be the first to offer such senior expertise to the country’s ambitious SMEs, is an innovative approach. By providing SMEs with access to a team of director-level experts with a hands-on ethos, we believe we can help our clients achieve and expand their goals.”

SSAS is a Belfast-based firm specialising in offering business owners tailored retirement schemes. Established in 2009 and now employing 12 staff, it provides pension administration and trustee services to more than 350 small self-administered scheme (SSAS) clients, with approximately £380m of assets under administration.

Director-owner Allison Chambers of SSAS expressed her appreciation of the role HNH played in the deal.

“We were delighted to work with the HNH team, who supported and guided us throughout the process. Their wealth of experience and negotiating skills were paramount in terms of the successful outcome,” she said.

This is the latest deal announcement in a sector for which consolidation has been a key recent theme. A trend that HNH believe will continue throughout 2019 and beyond.

“In recent months, we’ve seen Davy acquiring the former Danske wealth management business, 1825 acquiring BDO’s wealth management business and now Mattioli Woods acquiring SSAS Solutions,” said HNH Directors Richard Moorehead and Wayne Horwood.

“We were honoured to act as lead advisor to Allison and Michael and would be interested to speak with any other business owners in the sector who may be considering their options.”

Mattioli Woods said it will be business as usual for the SSAS Solutions team while it will also be looking to enhance the team as it expands its operations into the region, including the creation of a new administration hub for the group and the development of the existing client offering to include SIPPs (self-invested personal pensions).

“Being part of the Mattioli Woods group provides us with an additional resource and group support to enable the business to grow while still maintaining our strong client values, which also mirror those of Mattioli Woods,” said Allison Chambers and Michael Galway, director-owners of SSAS Solutions.

Mattioli Woods’ group managing director Murray Smith added: “We are thrilled to welcome the SSAS Solutions team into the Mattioli Woods family. A great opportunity to build on the success of an established business in Northern Ireland – where we already have a number of clients – we’ve known Michael and Allison for a number of years and have huge respect for the technical expertise their team offers.

“Their well-regarded skills and knowledge will be a valuable addition to our growing business, serving to further strengthen our services to clients and customers throughout Northern Ireland. We look forward to welcoming them to our expanding team.”

HNH are pleased to announce that Singapore Aerospace Manufacturing Pte Ltd (SAM) has completed its acquisition of JW Kane Precision Limited (JW Kane).

As lead advisor to the seller, HNH Director Wayne Horwood believes SAM’s foreign investment in Northern Ireland is another positive boost for the region.

“We’re delighted that SAM are investing in Northern Ireland and the future of JW Kane,” Horwood said.

“One of the benefits of SAM’s investment is to allow JW Kane to continue their good charity work throughout Northern Ireland.”

What is JW Kane?

JW Kane is a provider of supply chain solutions to the global Aerostructures industry.

Founded in 1984 by Mr James Walker Kane MBE and located in Northern Ireland, JW Kane utilise high speed machining technologies coupled with engineering know-how.

What is Singapore Aerospace Manufacturing?

SAM is a company incorporated and domiciled in the Republic of Singapore, providing precision engineering and equipment integration serving the global aerospace and industrial equipment arena.

The SAM Group of Companies have established operations in Singapore, Malaysia, Thailand, China and Germany.

Joining the family

“We are very excited to become part of the SAM family,” said Damian McArdle, JW Kane MD.

“Throughout the acquisition process, we could feel the synergy, vibe and energy working between our teams and it was a beautiful representation of the desired ‘beyond expectations’ performance that customers can anticipate from the new organisation,” he said.

“Never are we more certain of our capability to support customer demand and execute on our strategic growth objectives as part of the larger SAM group.”

“JW Kane is a terrific fit for SAM’s aggressive global growth strategy,” said Jeffrey Goh, SAM CEO and President.

With our plan to grow the capabilities and capacities in JW Kane, we will be able to offer more value added solutions to our customers in United Kingdom, Europe and the rest of the world.”

HNH Director Wayne Horwood

Wayne Horwood

Director

Email: wayne@hnhgroup.co.uk

Telephone: 02890 316931

We have been shortlisted in the Corporate Finance Team of the Year category. Craig Holmes features in the Dealmaker of the Year list. While, we were involved in a number of deals which have also gained prominence – the sale of fscom’s KYC Pro product to PWC, funding for ISL Waste Management Ltd (both feature in Deal of the Year – below £2.5m) and the acquisition of Alumasc Facades by Kilwaughter (Deal of the Year £2.5 – £10m).

“2018 was a fantastic year for HNH’s CF team, which nearly doubled in size from five to nine team members over the course of the year. As well as giving us crucial extra bandwidth, our targeted recruitment has added expertise in financial modelling, transaction services and debt advisory,” he said.

“We completed 15 transactions during 2018, covering a wide range of sectors and transaction types. Having three of our deals (Kilwaughter, FSCom and ISL) shortlisted for deal of the year is testament to the strength of our team and their hard work and dedication.

“2019 has continued in the same vein as 2018. At the end of last month, we completed the sale of the leading independent foodservice business, Foodco, to Henderson Foodservice and have another four or five deals scheduled to complete before the end of this quarter. ”

The annual NI Dealmakers Awards aim to recognise the high quality professional advisory firms and funders in Northern Ireland and some of the best deals in which they have been involved in over the previous calendar year. All winners will be revealed at the gala dinner event set to take place at the Stormont Hotel in Belfast on 14 March 2019.

The forthcoming Christmas break is, for many business people, the one time of year they can enjoy a proper break, away from the constant interruptions of emails and deadlines, and spend some quality time with friends and family, reflecting on the year just passed and the challenges that lie ahead.

This period of reflection is often the catalyst for change and we frequently find ourselves spending much of January meeting prospective clients who have expressed a desire to sell their business.

There are a number of valid reasons why someone may come to this decision including:

I have taken the business as far as I can.

My attitude to risk has changed.

The economy/competition/technology is a threat to me.

My team doesn’t have the ability to develop the business.

Multiples are strong in my sector and I want to get out at or near the top of the market.

I had an approach it has got me thinking.

I can’t work with my co-shareholders anymore and we need to go our separate ways.

Personal reasons such as a health scare or simply a desire to spend more time with family.

A key part of our process is to look beyond the headline reason for the decision and understand the underlying motivation.

We have bad days, or weeks, when work isn’t going well, the pressure is building and it just isn’t enjoyable.

However, for most business owners the decision to sell is a once or twice in a lifetime moment, so it is crucially important that proper consideration is given to the following thoughts:

Why now? What has changed in the business or personal circumstances?

What position is the business in? Does it need investment, new people, new systems, etc.?

What are the alternatives? Can something be changed that would take the pressure off and make work enjoyable again?

What could someone else do with the business? Are you selling an opportunity or a risk?

What will you do next? Even if the sale of a business yields a life changing amount of money, many sellers soon find themselves bored and seeking a new challenge.

It may sound counter-intuitive coming from a firm that ultimately gets paid when people sell their business, but we would much rather potential clients wait and sell for the right reasons, at the right time, rather than rush into a process which can be time-consuming, emotionally draining and indeed costly.

There is a high correlation between poor planning and aborted transactions; a failed process can linger over a business for years, putting doubt in the minds of employees, investors and potential acquirers.

Once the underlying reasons for wanting to sell are understood, only then should you look at the options, which may include:

A trade sale i.e. to another company.

A partial exit, achieved through selling a stake in the business to an investor, which would be a private equity fund, HNWI, family office, etc.

MBO, MBI or BIMBO.

Putting in place an exit readiness plan for a sale in the medium-term.

The Treasury has announced that the 2018 Budget will be delivered on Monday 29 October, a few weeks earlier than the November date which would ordinarily have been expected. Interestingly, this will be the first Budget delivered on a Monday since 1962, and the first delivered in October since 1945. Officially, the Treasury has said that this timing gives Parliament more time for debate before it rises for recess on 6 November – whether it also has anything to do with falling between two key Brexit summits in mid-October and mid-November is a matter for conjecture.

In accordance with the new Budget timetable the 2018 Budget will make the final announcement on measures to be introduced in Finance Bill 2018-19 and an initial announcement about measures which are being considered for Finance Bill 2019-20. A large part of the draft legislation for Finance Bill 2018-19 was published in July 2018 (and that after a period of consultation), so we have a good idea of what to expect. Some of the key changes are expected to be:

• An extension of the availability of Entrepreneur’s Relief to cases where an individual’s shareholding has been reduced below the 5% de minimis limit as a result of a dilution of his/her shareholding. This change is being implemented to avoid entrepreneurs being placed in a position where they are unwilling to seek additional capital for their businesses if this would jeopardise their Entrepreneur’s Relief position. The new rules will operate by way of two elections (the first being for a deemed disposal and reacquisition of the shares at market value immediately prior to dilution, and second for a deferral of the gain arising until an actual disposal), with the intention that the gain arising in the period up to dilution should qualify for Entrepreneur’s Relief. Following consultation, HMRC have confirmed that the market value required for the purposes of the first election will not have to take account of a minority discount (which would otherwise potentially disadvantage taxpayers). [Effective from 6 April 2019]

• The implementation of changes to bring UK property income of non-resident companies within the scope of UK corporation tax rather than income tax. Although the corporation tax rate applicable to such income is expected to be lower than the basic rate of income tax which is currently applicable (17% v 20%) and there will be provisions to allow existing income tax losses to be carried forward against corporation tax profits, this change will bring such companies within UK corporation tax rules for loan relationships (including corporate interest restriction and the anti-hybrids rules) which they hitherto would not have been required to consider. [Effective from 6 April 2020]

• Similarly, all non-UK resident persons will be taxable on gains on disposals of interests in any type of UK land, whether residential or non-residential – currently, such gains are only taxable (with some exceptions) for residential properties. The new rules will also give rise to a tax charge on indirect disposals of UK land, i.e. where a person makes a disposal of an entity that derives 75% or more of its gross asset value from UK land. There will be an exemption from this ‘indirect disposal’ rule for investors in such entities who hold an interest of less than 25%. [Effective from 6 April 2019]

• The disposal of a residential property by a UK resident will need to be reported in a return to HMRC, together with any applicable payment on account, within a ‘payment window’ of 30 days following the completion of the disposal. Certain non-UK residents are already required to make such returns and payments – the range of persons to whom these rules apply will be expanded. [Effective 6 April 2019 and 6 April 2020]

• The filing deadline for a Stamp Duty Land Tax (“SDLT”) return (and payment of related SDLT) will be reduced from 30 days to 14 days. [Effective 1 March 2019]

For further information or to discuss how the potential changes may impact you or your business, please contact Mark Hood, Director – M&A Taxation

HNH Group are proud to announce that we are sponsoring this year’s BVCA Belfast Business Breakfast.

As part of the British Private Equity and Venture Capital Association’s (BVCA) National Breakfast Series, we will be bringing together local private equity and venture capital communities from across Northern Ireland to share knowledge, forge new connections and network with fellow members.

Jointly sponsored by local law firm Tughans, the invitation only event will be held in the Merchant Hotel, 12th April 2018 and is exclusive to LP & GPs at BVCA member firms.

The business breakfast will run from 8-9.30am and will provide opportunities to explore the latest industry trends, economic developments and the work of the BVCA.

For availability and other enquiries please contact events@bvca.co.uk