Earlier today, Chancellor Jeremy Hunt delivered his second major fiscal statement in five months. With the OBR forecasting that the UK will not enter a technical recession this year (albeit it still expects a contraction of 0.2% in the economy) and that inflation will fall below 3% by the end of 2023, the Chancellor felt justified in saying that the UK economy was on the right track.

In terms of

specific policies, as is becoming the norm, the headline announcements have

been trailed in advance over the last few days. The main focus this year was on

expanding free childcare provision – while the key announcements applied to

England, they should lead to increased funding for Northern Ireland via the

Barnett formula.

Pensions Tax Relief

The main personal

tax-related announcement in this Budget was probably the changes to the pension

annual and lifetime allowances. The annual allowance (the amount which can be

contributed to pension schemes tax-free each year) will increase from £40,000

to £60,000 from 6 April 2023. The three year carry-forward of unused annual

allowances is retained.

The lifetime

allowance charge (currently applicable to pension pots in excess of £1,073,100)

will be removed from April 2023, with the lifetime allowance being abolished

from April 2024. However, the maximum tax-free lump sum that can be taken from

pensions at commencement will be retained and frozen at its current level of

£268,275 (i.e. 25% of the current lifetime allowance).

Capital Allowances

The Chancellor

committed to making the UK tax system one of the most competitive in the world.

He introduced two major capital allowances designed to boost investment.

Full Expensing

(“FE”) will allow companies incurring expenditure on capital allowance main

rate pool assets to claim a 100% deduction for the cost of the assets from

their profits. This FE will apply from 1 April 2023 to 31 March 2026 and will

result in a tax saving of 25p per £1 spent.

In addition, the 50% First Year Allowance (FYA) which is available on plant and machinery which qualify as special rate assets has been extended until 31 March 2026. For each year following the FYA claim, the remaining expenditure will continue to be written off at 6% per annum.

The

Chancellor’s long-term commitment is to make both these reliefs permanent.

However, while the £1m Annual Investment Allowance currently remains in place

indefinitely, we consider that the new relief will be of limited benefit to

most small or medium-sized businesses.

Research & Development

In the Autumn

Statement 2022, the government announced that from 1 April 2023 the rate of the

Research & Development Expenditure Credit (RDEC) for large companies would

be increased from 13% to 20%.

At the same

time a reduction in the Enhanced Expenditure Relief for Small and Medium size

Enterprises (SMEs) was announced, with the enhanced deduction for qualifying

expenditure reduced from 130% to 86% from 1 April 2023 and the payable credit

for loss making companies cut to 10% from 14.5% from the same date.

These changes

announced in the Autumn Statement will still come into effect on 1 April 2023.

However, today the Chancellor has announced an increased rate of relief for

loss-making R&D intensive SMEs. SME companies for which qualifying R&D

expenditure constitutes at least 40% of total expenditure will be able to claim

a higher payable credit rate of 14.5% for qualifying R&D expenditure

(resulting in £27 from HMRC for every £100 of R&D expenditure.)

The

implementation of overseas expenditure restrictions has been delayed for one

year and will now come into effect on 1st April 2024. This is to allow the

government time to consider the impact of this restriction on a single merged

R&D relief. The consultation on merging the R&D Expenditure Credit

(RDEC) and SME schemes closed on 13 March and draft legislation on a merged

scheme is expected to be published this summer for technical consultation.

Other Matters

The Budget was

noticeably light on mentions of income tax, national insurance contributions

and tax-free allowances –primarily because tax thresholds and allowances have

been frozen until 2027/28.

However, one other point of note for SMEs was the announcement of a relaxation of administration rules for Enterprise Management Incentive Schemes. From April 2023, there will no longer be a requirement for option agreements to include details of share restrictions, nor for a company to declare that an employee has signed a working time declaration. From April 2024, the deadline for notification of the option grant will be changed from 92 days following grant, to the 6 July following the end of the tax year in which the grant took place.

If you would like to discuss any of the above matters (or any other tax related issues) in more detail, please contact any member of our Tax team.

In

November 2022, the Chancellor delivered what was in effect a Budget in all but

name in which he cut spending and raised taxes in an attempt to reassure

investors about the UK’s commitment to financial stability. Given that

Government typically announces significant policy changes in the autumn and

lesser changes in the spring we are left wondering what Mr. Hunt will do on 15

March 2023 when he delivers his promised “full fat” budget and OBR Forecast. Whilst we can’t be certain what the

Chancellor will do, we do not expect major changes to the following reliefs and

incentives.

Seed Enterprise Investment Scheme (SEIS)

SEIS is a small-scale venture capital scheme designed to help start-up companies obtain initial investment. Amendments to expand the scheme were announced in the “mini budget” on 23 September 2022 and were one of the few announcements to escape the Government U-turn later in the year.

The new changes come into effect from April 2023 and provide for the following:

– The maximum amount a company can raise is increased from £150,000 to £250,000

– The gross asset limit will increase from £200,000 to £350,000

– The age of the new qualifying trade will increase from 2 to 3 years and

– The annual investor limit will double to £200,000.

For the investor with a stake of less than

30% in a qualifying company, SEIS can provide income tax relief of 50% of the

amount invested up to a maximum relief of £100,000. The relief can be claimed

in the year of investment, or any unused annual relief can be carried back to

the previous tax year. In addition, any

gain arising on the disposal of shares on which the investor received SEIS

income tax relief (which has not been withdrawn) is not a chargeable gain,

where the disposal takes place more than three years after issue.

Enterprise investment Scheme (EIS)

The tax incentives offered for EIS investments are intended to encourage investment in small, young high-risk companies which have limited access to market finance. There are stringent conditions attached to both the EIS issuing company and investor in order to obtain the relief. Originally EIS was subject to a sunset clause whereby the relief was to be no longer available for subscriptions made on or after 6 April 2025. The scheme has now been extended beyond 2025.

An investor subscribing for new shares in a qualifying EIS company can benefit from a number of reliefs including income tax relief up to 30% of the permitted maximum subscription, capital gains tax exemption, loss relief against capital gains or income tax and the ability to defer capital gains. In addition, Inheritance Tax Business Property Relief may also be available.

The permitted maximum investment in a qualifying company is £1m (or £2m where the investment is in a “knowledge intensive” company). However, the tax relief attaching to the investment can reduce a tax liability to nil but cannot generate a tax repayment so care needs to be taken not to invest more than the relief that can be claimed in the current or prior year.

Enterprise Management Incentive Scheme (EMI)

The need to attract and retain quality staff has always been important for employers but even more so in a competitive market where there is a skills shortage in the labour force.

EMI, which is tax advantaged share option scheme, is a selective share scheme allowing companies to target rewards to particular employees in order to drive performance and reward loyalty. With many businesses suffering from cash flow problems against a tide of rising inflation, offering non cash incentives to key employees may make leaving an employment a bigger decision than might otherwise be the case with a salary-only package. Employee share schemes can be used to create long term incentives typically aimed to crystallise on a sale or listing of the company, or alternatively as a reward for completion of a number of years’ service.

Share options allow employees to acquire shares at a fixed date in the future or following a predetermined event. The price they will pay for their shares is determined at the start of the process and employees have nothing to pay until they exercise the option and acquire the shares. No income tax or NIC is payable when the option is granted. Similarly, the exercise of the option should not give rise to an income tax/NIC charge (provided the various conditions of the scheme are met). Companies may also be able to claim a corporation tax deduction for the difference between the market value of the shares when the options are exercised, and the amount paid by the employee to acquire them.

The employees will be subject to capital gains tax when they sell the shares they acquire via the option but shares acquired via an EMI scheme may also qualify for Business Asset Disposal Relief resulting in a 10% capital gains tax rate on the first £1m of gains. This makes an EMI reward far more attractive from a tax perspective than a cash bonus on a sale of the company which would result in a tax charge of up to 47%.

Business Asset Disposal Relief (BADR)

BADR remains an important valuable tax relief – even after the reduction of the lifetime limit from £10m to £1m in March 2020. Originally called “Entrepreneurs Relief” it can be available on the disposal of a “business” such as a trading company, a sole trade business, share of a trading partnership or assets used by a trading company or partnership.

For shares in a trading company, the shareholder must hold at least 5% of the company’s ordinary share capital, voting rights, rights to dividends and assets on winding up at least 2 years prior to the sale as well as being an officer or employee of the company for an uninterrupted period of 2 years back from the date of sale.

Where the relief is available up to £1m of

capital gains will be subject to tax at 10%.

Inheritance Tax (IHT) and wealth management

IHT, sometimes referred to as the “death tax”, is charged at 40% on the excess value of a person’s worldwide non-exempt assets or “estate” (after deducting funeral expenses and debts) over the IHT threshold. As the threshold or the nil rate band has been frozen at £325,000 since 2009 and will be kept at that level until at least 2026, more people than ever may find themselves unexpectedly caught by this tax.

There are some steps that can be taken to help minimise any IHT exposure although generally IHT planning should take place earlier rather than later due to the 7-year cumulative clock on lifetime gifts that runs back from the date of death.

There are exemptions for IHT transfers between spouses i.e., those who are legally married to each other, those who are legally registered as civil partners and those who are legally married although separated at death. Individuals who are cohabiting are not considered spouses for IHT purposes.

Business Property Relief (BPR) is a very valuable IHT relief and usually applies to shares in trading companies. However, if the shares in a trading company are sold, BPR relief is lost, and the resultant sales proceeds could be exposed to IHT. Careful pre-sale planning can help mitigate future IHT risks.

If you would like to discuss any of the above matters (or any other tax related issues) in more detail, please contact any member of our Tax team.

The word ‘unprecedented’ can be overused in the modern world, but when

it comes to looking at events of the past few months associated with changes in

UK economic and tax policy, it seems particularly appropriate. In the Autumn of

2022, major tax changes were announced (and, in many cases, withdrawn) at a

pace never seen before.

While financial markets appear to have settled somewhat since the Autumn

Statement delivered on 17 November, there might easily be some confusion as to

what the current position is with respect to those matters which were subject

of discussion.

Therefore, it is worth taking stock of where some of those key matters now stand. What follows is a brief summary of some of the main points, setting out what the current position is.

1. Capital Gains Tax (“CGT”)

The headline announcement was that the Annual Exempt Amount (“AEA”) will

be reduced from £12,300 to £6,000 in April 2023, before being further reduced

in April 2024 to £3,000. Key reliefs remain available (e.g. Business Asset Disposal

Relief and Investor Relief.) There are no indications whether the rates will increase

in the short to medium term but for now they remain unchanged and are still

relatively low:

Band

Rate

Basic Rate Band

Residential Property Gains

18%

All other gains

10%

Higher Rate Band

Residential Property Gains

28%

All other gains

20%

The current capital gains rates are still attractive compared to the

much higher income tax rates. There may also be merit in maximising the AEA by

timing smaller disposals to happen before the reductions begin in April 2023.

2.National Insurance Contributions (“NIC”)

Perhaps the source of the greatest confusion has been the increase in national insurance rates and the introduction of the Health and Social Care Levy (“HSCL”) in April 2022, followed by their withdrawal from 6th November 2022.

The amount at which an individual employee starts to pay NIC was aligned

with the Income Tax Personal Tax Allowance from 6th July 2022

(£12,570). The rate at which employers start to pay NICs is £9,100.

Details of the rates and bands applicable throughout the year are set out in the Appendix at the end of this article.

There is also a hybrid rate for Class 1A NIC for the full tax year ended

5th April 2023 in relation to expenses and benefits, and Class 1B

NIC in relation to PAYE settlement agreements – this rate is 14.53%. This is

also the rate for directors cumulative NIC calculations for 2022/23.

Dividend rates increased from 6th April 2022 in tandem with

the NIC rates, by 1.25% each. However, unlike the NIC rates, these were not

reduced in the Autumn Statement. Rates remain 8.75% for basic rate band

dividend income, 33.75% for higher rate band dividend income and 39.35% for

additional rate dividend income. The dividend allowance is to be reduced from

£2,000 to £1,000 from 6 April 2023 and then to £500 from 6 April 2024.

3. Off Payroll Working (“OPW”) Rule

Most businesses would have breathed a sigh of relief when the “Mini-Budget”

announced the reversal of the extension to the OPW rules (by abolishing the new

rules brought in from April 2017 and April 2021), returning the responsibility

for operating PAYE/ NICs to the Personal Service Company (“PSC”) itself.

Their relief was to be short-lived though, as, soon after taking office

as Chancellor, Jeremy Hunt announced that these new rules were not to be

abolished.

Under the

Off-Payroll Working Rules it is the company to which the worker or director

provides their services (i.e. the client) that has responsibility for making

the Status Determination Statement in respect of the worker, with the fee-payer

(and not the PSC itself) having responsibility for deducting the tax and

NIC liability via payroll, if the relevant employee is found to have employee

status for tax purposes. The rules apply if a worker provides their services to

a client through an intermediary but would be classed as an employee if they

were contracted directly. Initially, the

new rules only applied to public sector clients from April 2017, but from 6

April 2021 they extended to clients in the private sector that are medium or large.

Where a contractor

is working for a small client entity the OPW rules continue to apply as prior

to April 20017 in respect of potential deemed employment relationships, i.e. it

is the PSC which has any responsibility for paying PAYE/ NIC to HMRC.

4. Research & Development (“R&D”) Changes

Changes to the R&D schemes were not unexpected following the 90% increase in R&D enquiries amid HMRC’s continuing concerns over the level of error and fraud in R&D claims. It is hard to see however how the changes introduced can be used to prevent fraudulent claims. Changes to both schemes from 1st April 2023 are as follows:

SME incentive scheme:

– Additional deduction reduced from 130% to 86%

– SME tax credit reduced from 14.5% to 10%

RDEC incentive scheme:

– RDEC rate increased from 13% to 20%

Further measures to tackle fraud in R&D claims have been set out in draft legislation, intended to be introduced from April 2023, and include the requirement to name the adviser preparing the R&D report on the claim, the requirement to make advance notification of a claim and the requirement to have the claim signed off by a senior officer of the company. The requirement to name the adviser compiling the report will presumably help HMRC develop a list of trusted agents which could then expedite some claims, freeing up HMRC staff to enquire into the higher risk claims.

5. Stamp Duty Land Tax (“SDLT”)

On 23rd September, Kwasi Kwarteng announced, as part of his

Growth Plan, the doubling of the stamp duty threshold to £250,000 and increased

the threshold for first time buyers from £300,000 to £425,000 and increased the

maximum property value for first time buyers from £500,000 to £625,000.

There had been no time limit placed on these threshold extensions, however Jeremy Hunt has now confirmed in his Autumn Statement that this will be a temporary measure, ending on 31 March 2025.

6. Surviving from the Growth Plan

Between the Growth Plan Statement and the Autumn Statement many elements

of the former were quickly dropped. To try to stabilise the markets the

abolition of the additional rate band was abandoned (with the Autumn Statement

increasing the band of income which will be subject to the additional rate),

the cancellation of the increase in corporation tax was set aside, as was the

cancellation of the increase in dividend tax rates. Not all elements of The

Growth Plan were scrapped though, as set out below:

– The permanent increase of the Capital Allowances Annual Investment Allowance to £1 million remains

– The increase in the Company Share Option Plan Limit from £30k to £60k will go ahead

– The increase in the amount of SEIS investment companies can raise (from £150k to £250K) has been retained

– The Health and Social Care levy remains cancelled.

It is to be hoped that, following an Autumn of significant upheaval for the Government – in terms of both economic policy and personnel – there will be a period of relative calm which will allow businesses to adjust to the new landscape. However, there are no guarantees of this in the current climate and businesses will need to remain adaptable in the face of ongoing political and economic uncertainty.

If you would like to discuss any of the above matters (or any other tax related issues) in more detail, please contact any member of our Tax team.

Appendix – NIC rates and band applicable in 2022/23

The rates for 2022/23 are as follows:

6th April 2022 – 5th July 2022

Band

Percentage

Employee Contributions

Between £12,570 and £50,270

13.25%

Over £50,270

3.25%

Employer Contributions

Over £9,100*

15.05%

6th July 2022 – 5th November 2022

Band

Percentage

Employee Contributions

Between £12,570 and £50,270

13.25%

Over £50,270

3.25%

Employer Contributions

Over £9,100*

15.05%

6th November 2022 onwards

Band

Percentage

Employee Contributions

Between £12,570 and £50,270

12.00%

Over £50,270

2.00%

Employer Contributions

Over £9,100*

13.8%

*Disregarding the exemption for employer’s

contributions in relation to employees under 21 years of age.

Due to ongoing growth in our Business Advisory Services Practice (“BAS”), we are now looking to recruit a graduate to join the firm on a 3.5 year training contract, during which time they will undertake professional studies towards becoming a chartered accountant with Chartered Accountants Ireland. The successful candidate will report to the BAS management team and will be involved in the provision of advisory and restructuring services to a wide range of stakeholders, including banks, funds, alternative lenders and corporates. The role will include the following:

Provision of professional advice and services to a wide ranging portfolio of clients, to include:

Turnaround options advice and business restructuring;

Debt and refinancing advice;

Accelerated M&A;

Independent Business Reviews;

Corporate simplification;

Corporate insolvency;

Personal insolvency;

Forensic services, including litigation support, expert witness services and financial investigations; and

Business intelligence services.

Essential Criteria

Recent graduate with First Class or 2:1 Honours Degree (or equivalent), preferably in finance / accountancy or a business related degree, however all degree types will be considered;

Intention to pursue and obtain professional exams;

Confident with Microsoft applications including Outlook, Word, Excel and PowerPoint;

Excellent communication, presentation and interpersonal skills;

High attention to detail and accuracy;

Commercial awareness;

Strong work ethic;

Team player;

Proactive and positive approach including ability to use own initiative; and

Time management skills.

This is a full time position and will be based in our Belfast office.

Although described as a ‘mini-Budget’, the Chancellor’s Statement on The Growth Plan 2022 earlier this morning introduced a wide range of measures. In addition to attempts to deal with rising energy prices, the Government set out a range of tax cutting and other incentive proposals with the key aim of stimulating economic growth. The main tax-related measures are noted below:

Income Tax and NIC

The Basic Rate of Income Tax will be cut from 20% to 19% from April 2023.

The temporary increase in NIC of 1.25% is to be cancelled effective from 6th November 2022. The 1.25% increase in dividend rates will be cancelled from April 2023. The Health and Social Care levy, which had been proposed for introduction in April 2023 has also been cancelled.

The government will also abolish the Additional Rate of Income Tax such that, with effect from April 2023, there will be a single higher rate of Income Tax of 40 per cent, rather than an additional 45% on annual income above £150,000.

Corporation Tax

There will no longer be an increase in the headline corporation tax rate to 25%, keeping the rate at 19% after 1st April 2023.

The reduction in the level of Annual Investment Allowance is also cancelled, with the relief now available permanently on £1 million of qualifying expenditure on plant and machinery per year.

Stamp

Duty Land Tax (SDLT)

The government is reforming SDLT in England and Northern Ireland by doubling the level at which people begin paying this from £125,000 to £250,000 from today.

There are also increases in reliefs offered to first time buyers- by increasing the level first-time buyers start paying SDLT from £300,000 to £425,000, and by allowing them to access the relief when they buy a property costing less than £625,000 rather than the current £500,000.

Other Matters

With effect from April 2023 the government will repeal the off-payroll working (i.e. IR35) reforms introduced in 2017 and 2021. This will once again leave the primary responsibility for determining employment status (and also operating PAYE and NIC) with the personal service company, rather than with the client/ engager.

Company Share Option Plan limit increased from £30k to £60K from April 2023

The amount and availability of the Seed Enterprise Investment Scheme (SEIS) will be increased, with companies able to raise up to £250k of SEIS investment, increased from £150k.

The government remains supportive of the Enterprise Investment Scheme (EIS) and Venture Capital Trusts (VCT) and sees the value of extending them in the future.

Businesses in designated “Investment Zones” will benefit from time-limited tax benefits in England, including enhanced capital allowances, structure and buildings allowances, business rates relief, Employers NIC relief and SDLT relief. The government intend to work with devolved administrations to develop similar opportunities in Northern Ireland, Scotland and Wales.

The measures outlined today went further than what had been

trailed in the press over recent days and it obviously remains to be seen

whether they will have the desired effect. However, it would be fair to say

from the outset that the desire to simplify the IR35 rules will be welcomed, as

these have been causing significant uncertainty for businesses in recent years.

HNH are delighted to welcome Connor McAnallen as a Manager into our Deal Advisory team.

An Accountancy graduate of Queens University Belfast, Connor completed his training contract within the Accounts and Business Advisory Department of RSM in Belfast before moving to the Corporate Finance team within Mid Ulster based CavanaghKelly. During this time, he has gathered experience in both M&A lead advisory work as well as the delivery of due diligence projects.

Rodney McCaughey, Transaction Services Director welcomed Connor to the team, saying, “We are delighted to welcome someone of Connor’s calibre to the deal advisory team, and we are confident that the skills and experience he brings will make a significant contribution in delivering our growth plans.”

Connor added, “I am excited to take up my new role within HNH and look forward to working with the firm’s wide variety of quality clients. I am also looking forward to working alongside a team of top tier finance professionals to build on my experience gained to date in my career.”

HNH are delighted to welcome Matthew Mitchell to our Business Advisory Services team.

A graduate from the University of Ulster, Matthew recently achieved a first-class honours in Business with Accounting and joins the BAS team as a trainee accountant.

Matthew spent a placement year with Ulster Bank in Belfast and continued to work there part-time alongside his final year studies.

James Neill, Head of BAS, said: “We are delighted that Matthew has agreed to join the team at HNH. His addition to the team, further enhances the strength and breadth of our BAS department”.

Matthew added, “I am delighted to have this brilliant opportunity as a trainee accountant at a dynamic, growing business. I am looking forward to working with experienced individuals, and a variety of people and organisations, whilst garnering expertise in a range of areas.”

“With increasing concerns around climate change and the cost of energy, it’s no surprise to see growing appetite for investments in the renewable energy sector.”

Following the successive recent completions of the debt funded MBO of Realise Energy Services Ltd[i], and the investment into The Electric Storage Company[ii], HNH’s Head of Sustainability, Paul Gleghorne gives his thoughts on transactional activity for companies operating within the renewable energy sector.

“We have had an incredibly busy M&A market generally for

12-18 months, with a multitude of transactions across a range of sectors. The

rhetoric from institutional investors remains positive around the availability

of capital and their desire to deploy through all cycles. M&A activity and

investments will continue but with a combination of cost inflation, supply chain

issues, geopolitical uncertainty, and the remnants of COVID-19, we expect deals

to be more strategic and measured, where strong management teams and deal

structuring are likely to be key factors. Opportunities within defensive

industries, especially where regulation is driving investment, will remain

attractive.”

Paul explains that appetite for opportunities in the

renewable energy sector has remained particularly high.

“The steep rise in the cost of energy has highlighted the overreliance

on conventional energy generation. Many large energy users are now seeking to

lower their marginal cost of energy use by installing solar panels and

batteries or even opting to build their own renewable energy generation as

private wire projects. In addition, it is becoming increasingly important for

companies to demonstrate their green credentials to customers with ESG

reporting requirements. On the other side, whilst financial returns ultimately

drive decision making, investors are becoming increasingly eager to provide funding

or invest in opportunities which assist in achieving their ESG targets.”

“It’s not all asset-based investments either, there are a

host of companies providing services that facilitate the use of renewable

energy. The recent deals of Realise Energy Services, who operate and maintain over

200 wind turbines across the UK, and power engineering and technology business The

Electric Storage Company, attracted considerable interest with some interested

parties citing green credentials as a contributing factor in their decision

making.”

HNH Corporate Finance have a dedicated team with a specific

focus on transactions in the sustainability sectors, ranging from sell/buy side

M&A, raising project finance and appraising investment opportunities.

[i] The

MBO of Realise Energy Services Ltd was funded by specialist credit provider

Beach Point Capital

HNH are

delighted to welcome Lucas Batchelor as an Assistant Manager to our Deal

Advisory team.

Lucas graduated

from Queen’s University Belfast with first class honours, completing a BSc in

Economics with Finance. During his time at the university, he was awarded the

prestigious Porter Scholarship. Lucas completed his training as a chartered

accountant in KPMG’s audit team in Belfast. He is currently completing an MSc

in Data Analytics at the University of Glasgow and has recently submitted his

final dissertation, “Comparing the performance of bankruptcy prediction

methods”.

His appointment

illustrates the continuing expansion and development of the Deal Advisory team.

“Paul Gleghorne commented: “We are delighted to further bolster our team

within the Corporate Finance and Financial Modelling service lines. Whilst

2022/2023 will have more complexities for those considering embarking on

M&A, we have an exciting pipeline of work and this is a sign of continued

investment in our growing team.”

Lucas said, “I

am thrilled to begin my new role within the Deal Advisory team at HNH. I am

looking forward to working with a wide variety of quality clients and

continuing my professional development within a team of high calibre

individuals.”

HNH are delighted to welcome Caoimhe Sweeney as an Assistant

Manager into our Business Advisory Services team.

A law graduate of Queen’s University, Caoimhe then qualified

as a chartered accountant while working within Ernst & Young’s tax

department.

John Donaldson, Director within Business Advisory Services

said, “We are delighted to welcome Caoimhe into our team and believe that her

legal and tax experience will be a great addition to the existing skillset

within the department.”

Caoimhe said, “I am very excited to begin my new role within

HNH and look forward to working with businesses and individuals as they

navigate the post-COVID landscape.”

With the Chancellor’s Spring statement fast approaching, those

business owners contemplating retiring or exiting their business will no doubt

be considering the possible implications for them should the Government announce

changes to the Capital Gains Tax (‘CGT’) regime.

As the Government continues to deal with the aftermath of unprecedented

borrowing to support the economy during the pandemic, some consider that CGT

could be next on the Chancellors hit-list to raise funds. This could be

achieved through the removal of business asset disposal relief (‘BADR’) or, as

recommended by the Office of Tax Simplification, increasing the CGT tax

rate.

Business owners can mitigate their risk now by discussing a Members’

Voluntary Liquidation (‘MVL’) with an Insolvency Practitioner to explore

whether it is an option suitable for them.

An MVL is an option for solvent companies wishing to wind down their

activities and allows for assets to be distributed in a tax-efficient manner,

whilst also giving directors certainty given the finality of the liquidation

process. Subject to certain conditions, distributions made in an MVL can

qualify as capital distributions and business owners can avail of BADR with a

tax rate of 10%. At current rates, this relief can save business owners up to

£100,000 in CGT.

An MVL is only an option for solvent companies meaning that the company

must hold enough assets to be able to settle all liabilities and interest in

full, normally within 12 months. Due to the

ability under company law to hold members’ meetings at short notice, companies

can often be placed into an MVL within a couple of days.

While no-one really knows what the Chancellor’s plans are for CGT come

23rd March and beyond, business owners should always keep one

eye on their exit strategy and plan accordingly. This will ensure their

company’s activities are wound down in the most efficient possible manner.

If there has one benefit from

the past 2 years, it is undoubtedly the opportunity to spend more of those

precious moments with our kids. Whether that be the school run, homework or

generally just being around more, the pandemic has afforded people the

opportunity to reset and perhaps realign those priorities in life.

I’m sure like many, after an

excitable day, our kids like to unwind before bedtime with a book.

During a recent reading of Julia

Donaldson’s “A Squash and a Squeeze”, I’m sorry to admit, but my mind started

to wander as I was reciting the words (almost by memory now at this stage!).

With the increase in hybrid

working, I’m sure many might relate to the challenges of space being at a

premium in our households at times, however I then began to consider the

current fiscal squeeze facing many households.

Fiscal Squeeze

Whether it be rising heating bills, electricity costs, shopping bills, credit cards or fuel costs, the squeeze on household income is very much real.

Coupled with future increases in National Insurance Contributions from 6th April 2022 as well as last week’s announcement of future increases in local property rates, the financial pressure facing households continues to increase.

It was recently reported by

the Office for National Statistics (“ONS”) that 76% of people were paying more

for food, energy and petrol in the 10 days 3rd February 2022 to 13th

February 2022. This was an increase from 69% for the period 19th

January 2022 to 30 January 2022. Furthermore, consumer prices also rose by 5.5%

in the 12 months to January 2022, the highest since March 1992 (7.1%).

The challenges presented by such inflation cannot be underestimated.

Whilst the Bank of England have attempted to curb the rising levels of inflation by increasing interest rates earlier this month, this will also have an additional knock-on effect on those with tracker or variable rate mortgages, further tightening the squeeze facing many household incomes.

Not Just Households, Businesses Too

Of course, this pressure is not limited to purely households, with many businesses also facing rising costs.

Inflation, Brexit and wider

economic and political issues have resulted in increased labour, transport and

material costs. The resulting impact on margins has been considerable for many

businesses, and whilst many have publicly stated that every effort is being

made to avoid passing such cost increases on to the consumer, the above ONS

statistics unfortunately confirm the reality that such costs are already being

passed on and will likely continue to be in the months ahead.

Plan, Plan, Plan

For both consumers and businesses, the only response to such rising costs is to plan accordingly.

Households should start, or if they already have one, update, their household budget. This will not only help prioritise essential expenditure and manage outgoings, but also highlight any potential areas of concern. Once highlighted, any such problems can then be addressed at an early stage before they become too problematic.

Similarly, businesses should

review their business plan and update their financial projections accordingly.

Owners should perform extensive

sensitivity analysis under various scenarios and take time to strategise

regarding both the pressures currently being faced and the future direction of

the business as a result.

Again, early phase planning and review, will help businesses identify any funding gaps or financial pressures, which can then be discussed with stakeholders, banks, funders and / or creditors.

What is important to note

however is that no matter how big the problem may seem, there is always

professional assistance available to help work through the issues.

Advice

Seeking the assistance of

professional advisors to review and critique a household budget, or a business’

operational, financial and strategic plan, could provide the very solution to the

current pressures being faced.

There are solutions out there

that can provide a chink of light in even the bleakest of situations. What is

required is early engagement to identify and address the issue, and a focused and

tailored approach to its resolution.

Whilst the past few years have presented their challenges, we all must recognise of how far we have come and what we have all been through. Of course, there will be further challenges ahead and we are all aware that the unprecedented level of Government support during the pandemic will have come at a cost.

However, if we all face this current period with the same approach and determination that we have recently shown, people and businesses can come through this and be in a position to take advantage of future opportunities that present themselves.

HNH are delighted to welcome James McMullan to our Business

Advisory Services team.

A graduate from Queens, James has recently completed his

MBA at the University of Ulster and joins the BAS team as a trainee accountant.

James’ addition brings the overall BAS headcount to over 10

and represents yet further investment in HNH’s BAS offering.

James Neill, Head of BAS, said: “We are delighted that James

has agreed to join the team at HNH. His addition to the team, further enhances the

strength and breadth of our BAS department”.

James McMullan added: “I’m very pleased to have joined the

BAS team at HNH during this exciting period of growth and am looking forward to

working with our range of clients on a variety of advisory projects.”

HNH acted as Lead Corporate Finance Advisor for

rapidly growing eCommerce business Candle Shack in a £4.4m deal. Candle Shack,

founded by Duncan and Cheryl MacLean in 2010, supplies candle making components as well as providing contract

candle manufacture for high profile, luxury brands. The transaction includes £3

million of funding from Maven’s high net worth investment syndicate, Maven

Investor Partners, as well as a £1.4 million debt facility from HSBC.

Neal Allen, Director in the Corporate Finance team

at HNH, said: ‘One of the reasons that we established HNH in Scotland was to

advise exciting, fast growing businesses and it has been fantastic to work with

such a great example in Candle Shack. The deal is a validation of not only all

of the inspiration and perspiration that Duncan and Cheryl have put in over the

last few years, but also of the Scale Up programme and the next wave of

entrepreneurs that are helping to drive the Scottish economy forward. ‘

Candle Shack employs 105 staff and operates

from its 100,000 ft2 West Carron facility in central Scotland encompassing a fulfilment

centre, development lab and manufacturing. The Company provides everything for

an artisan manufacturer to make high quality candles, including fragrances,

waxes, wicks, glassware, and bespoke branded packaging. Making fine candles is

a technical endeavour and many of Candle Shack’s customers rely on the business

for support, training, accreditation and for the testing of their candles. In

addition, the company serves clients who require contract candle manufacturing

services where the company deploys state of the art technology and artisan

craftsmanship to produce candles for some of the world’s leading luxury

brands.

The company is regarded as the market leader in

Europe currently serving over 34,000 loyal customers and has a reputation for

high quality products and excellent customer support. Candle Shack has enjoyed

strong sales growth over recent years benefiting from its focus on the premium

and artisan segments of the market. Consumers are looking for unique, locally

produced premium products at affordable prices and this is increasingly being

met by artisan candle makers many of whom are Candle Shack customers. The

company is also working hard to offer candle ingredients that are sourced

sustainably, and this includes its best-selling own-brand, environmentally

friendly wax blend.

Maven’s support will enable management to

further scale the business, investing in new marketing and sales channels,

expanding its EU operations, financing further product development, and

improving operational efficiencies to enable Candle Shack to grow its customer

base, broaden its offering and continue to offer customers a best-in-class

service.

Duncan MacLean, CEO at Candle Shack, said: “Maven’s

investment in Candle Shack will fuel our next phase of growth, increasing our

ability to support thousands of niche home fragrance brands across Europe. We

are excited to be partnering with such an experienced investor and with Maven’s

support, are aiming to cement our position as Europe’s leading home fragrance

supplies business.”

We are delighted to announce the promotion of John Donaldson to Director within our Business Advisory Services (BAS) team.

James Neill, Head of BAS & John Donaldson

James Neill, Director and Head of BAS said, “John’s hard work and dedication has been evident from the moment he joined the firm. He is a valuable addition to the HNH Board, bringing with him over 20 years of experience working within the corporate advisory and restructuring space. This promotion continues to demonstrate HNH’s core ethos of providing our clients with experienced, director-led support”.

John added, “Having joined HNH a year and a half ago, I am extremely excited and proud to take up my new position on the Board and look forward to continuing to work with the wider team and our existing clients to further enhance HNH. With the Northern Ireland economy going through a period of constant change over the past couple of years, the experience and depth of the team within HNH, together with our diverse product offering, will put us in a strong position to help our clients deal with the ever evolving marketplace.”

John is a Fellow of the Chartered Accountants Ireland and a licenced Insolvency Practitioner.

HNH acted as Lead Corporate Finance Advisor for Powerhouse. HNH

Head of Sustainability, Paul Gleghorne, commented “HNH were delighted to act

for the company on this transaction. Powerhouse provides vital services to

facilitate renewable energy on the grid and reduce energy demands of large

consumers. The acquisition by Cool Planet Group will facilitate the growth of

the company’s services in the sector.”

Powerhouse Generation Ltd was founded in 2013 as a DSU

aggregator operating within Ireland’s electricity market. Since inception,

Powerhouse has added DS3 trading and consultancy services to its offering.

Powerhouse Energy Management Ltd was setup in 2019 and acts as an advisor and

broker in the energy sector giving Powerhouse a full suite of energy management

services.

HNH Head of Deal Advisory, Richard Moorehead, stated “this

transaction is indicative of HNH’s increased focus on working with companies in

the sustainability sectors, including renewable energy and waste management.

These sectors are key growth areas for HNH and we are continuing to grow our Sustainability

team in Belfast.”

Commenting on the acquisition, Richard Watson, Chairman of

Powerhouse, said “we are looking forward to working with Cool Planet Group and accelerating

our growth plans and expansion into new markets.”

Alan Keogh, chief executive of Crowley Carbon, says Powerhouse’s

“demand response capabilities will compliment our existing offerings of solar

PV, battery storage, electrification of heat, EV chargers and vehicle to grid,

enabling us to reduce carbon and greenhouse gas emissions in plants for a net

zero future. We can now create new offerings that combine energy efficiency,

renewable power, EV-charging and sustainability and compliance reporting to

help organisations reach their net-zero carbon goals.”

Tughans in Belfast, led by James Donnelly, acted as legal

advisors to Powerhouse.

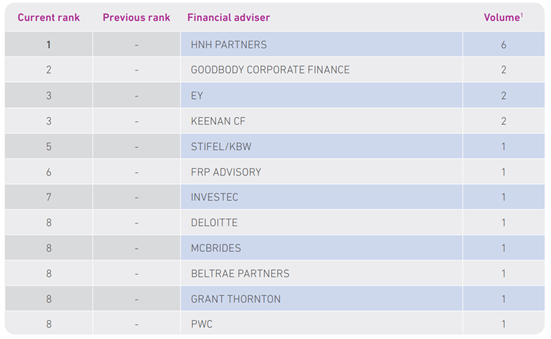

With the publication of the latest Experian M&A League Tables, we are very pleased to report that our Deal Advisory team in Northern Ireland has maintained its position as the leading corporate finance advisor in the region, closing nine deals in the first half of the year.

Our Scottish team continued its strong start to the year, closing seven transactions throughout H1.

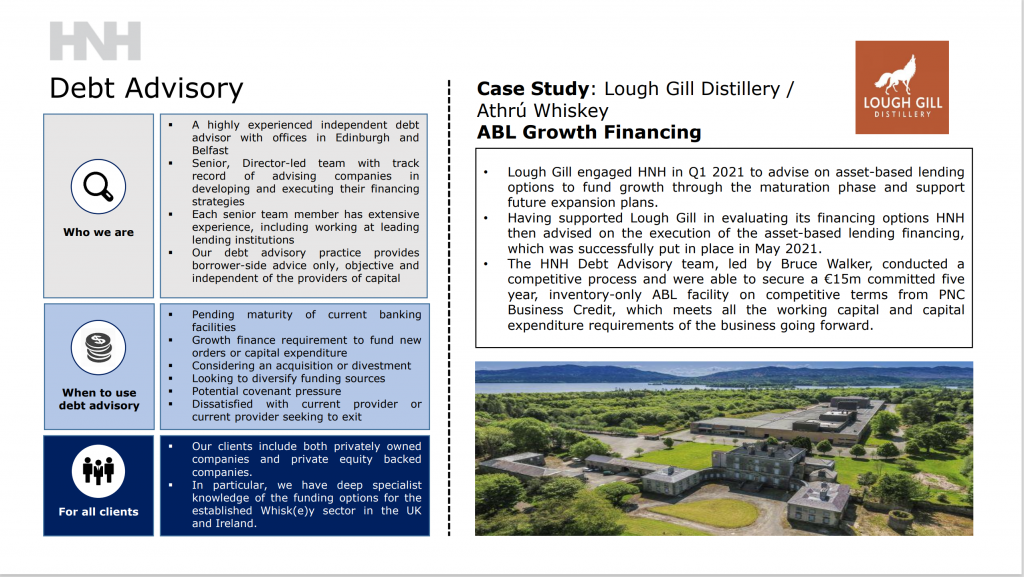

A Debt Advisory team, led by Bruce Walker recently advised Athru Whiskey on a £15m ABL fundraise from PNC. This is the fourth funding round we have advised on in the whisky/whiskey sector in the past 12 months and the first involving an Irish whiskey.

Of particular note is that the collateral available to the lender in this case was primarily new make spirit; hitherto, some lenders had been reluctant to fund the maturation period for new make spirit and we therefore view this as a landmark transaction, in particular for the growing Irish whiskey sector.

It gives us great pleasure to announce that Rory Moynagh, Associate Director in our Business Advisory Services (BAS) department, has successfully passed both the JIEB corporate and personal examinations and is now qualified to become a fully licensed Insolvency Practitioner (IP).

This is a fantastic

achievement especially in light of the fact that Rory was the only person in

Northern Ireland to successfully pass both exams in 2021, the extenuating

circumstances of studying during a lockdown period and a very challenging

examination with a low pass rate throughout the UK.

James Neill, Head of BAS,

commented:

“We are very proud of Rory’s

achievements and he deserves a massive congratulations for the hard work he put

in throughout 2020. As demonstrated by the final results, this was a very

difficult JIEB sitting in an extremely challenging time.”

“Rory is one of our longest serving employees, in fact he was HNH’s sixth ever employee, so it’s been a pleasure to watch Rory’s career develop over the years, and all of us at HNH are delighted at his recent success. We look forward to him becoming a fully licensed Insolvency Practitioner and further strengthening our client offering. To have 4 licensed IPs in HNH helps highlight the strength in depth we offer within the wider BAS team.”

Rory joins the firm’s existing licensed Insolvency Practitioners, James Neill, John Donaldson and Cathy McLean.

We are delighted to see the efforts of our deal advisory teams in NI and Scotland recognised by their strong showings in the Experian UK & RoI M&A League Tables for Q1 2021. Our NI team was the most active in the country, completing six transactions in the quarter, while our Scottish team narrowly missed out on top spot, closing three deals in the period.

As a result of our ongoing expansion, we are now looking

to appoint a Business Support Assistant. The successful candidate will be the

first point of contact for clients and be the face of the business. This

individual will report to the Finance Director and will support them in the

operational management of both offices. This individual will have exposure to

all operational aspects of the business and senior staff. This is a key role

for the organisation and this individual will be integral to driving

initiatives and efficiencies throughout the business.

Typical duties will include:

Front of house – greeting clients,

answering phone calls, organising meeting rooms and preparing and distributing mail.

Finance assistant – supporting the

Finance Director in maintaining financial records to include completing daily

bank reconciliations, recording supplier invoices, generating client invoices, preparing monthly payment runs, processing employee expense claims and filing documentation as required.

HR and Personnel – Co-ordinating travel,

accommodation and conference requirements for employees and visitors, supporting staff in the co-ordination of external marketing events, assisting with the onboarding of new staff and supporting the Finance Director in the monthly payroll process (to include the management of annual leave).

IT and Property – Managing and re-ordering of office stationery and office supplies, supporting staff to resolve day-to-day IT issues and building relationships with key suppliers.

The above list of duties is not exhaustive, and the

individual may be required to undertake other tasks as directed by the Finance

Director.

Essential Criteria

Minimum of 2 years’ work experience in a similar

role.

Confident with Microsoft applications including

Outlook, Word, Excel and PowerPoint.

Experience of finance-related administration.

Strong verbal and written communication skills.

Excellent planning and organisational skills to

include demonstrable experience coordinating internal and external events.

Confidence to work with and take instruction

from all stakeholder levels.

Strong attention to detail.

Ability to work independently, but also collaboratively as part of a team.

Ability to work efficiently and prioritise work

as needed.

Desirable Criteria

Experience working within a similar professional

service environment.

Experience of HR related administration to

include payroll.

Experience of marketing related administration.

Experience with Xero accounting software.

This is a full time position and will be based in our

Belfast office. Remuneration will be in the region of £18-22k per annum

depending on experience.

To apply for this position please submit a CV by email to careers@hnhgroup.co.uk by no later

than 1700 on Friday the 9th of April 2021. Where possible, you

should state any experience you have had, which shows how you meet the criteria

specified above, when you submit you CV application.

The Deal Advisory team at HNH is delighted to announce two pieces of good news:

Chris Hylands joined the team in December 2018 and, over the past two and a bit years, has worked on a wide range of transactions across NI and Scotland. In recognition of his hard work and technical development, we are very pleased to announce his promotion to manager, effective 1 April.

On the other side of the Irish Sea, we welcome Craig McGill to the Edinburgh office. Craig joins us as an assistant manager and brings the team in Scotland to five. His appointment comes at a good time with activity levels building strongly this year and continuing the trend that we started to see in the final quarter of 2020.

Earlier today the Government issued its ‘Tax Policies and

Consultations’ document. There was speculation that this would be the

opportunity for the Government to signal future tax changes (and for that, read

tax increases) that would take place in the coming years.

This document, in the form of a command paper, announced

approximately 30 Government consultations which would normally have been

published at the time of the Spring Budget. However publishing these documents

post Budget is a new approach by the Government as part of the 10 year tax

administration strategy they produced last summer. The Government’s objective

is to build a trusted, modern tax administration system to facilitate tax

policy development across a range of important tax issues covering rapid

social, economic and technological change, whilst seeking to create greater

visibility and transparency for parliamentarians, tax professionals and other

stakeholders. The Government’s hope is that increased scrutiny of tax measures

will increase the overall quality of tax policy and legislation.

So with all that now explained, was there anything of

note in the documents published today? In simple terms there were no real

headline grabbing announcements which will result in immediate tax changes.

However, there are some noteworthy proposals that have been put out for consultation

which will have a medium to longer term impact on business.

In terms of tax administration, the clear direction of

travel is towards continued digitisation. The ‘making tax digital’ process for

VAT has been regarded as a success and the Government intends to carry on with

its introduction to the income tax self-assessment system. The Government has

further committed to investing into the digitisation of the tax administration

infrastructure so that each citizen will end up with a ‘single digital account’

and a ‘single digital record’. There are also consultations on raising the

standards in the ‘UK tax advice market’, including the proposal that all tax

advisers should have professional indemnity insurance and recommendations that

the reporting of inheritance tax should be significantly simplified in respect

of estates for which no inheritance tax is due.

No Government fiscal announcement would be complete

without the ubiquitous tackling of ‘non-compliance’. There are further

consultations on clamping down on the promoters of tax avoidance and tackling disguised

remuneration, which normally takes the form of non-taxable loans being issued

to employees instead of salary or bonuses. There is the publication of some

research on the impact of the ‘off payroll working’ rules (known as IR35) which

were introduced into the public sector in 2017 and which are coming into the

private sector in April 2021 – but there is no indication of the latter reforms

being delayed. There is also a consultation on making the renewal of certain Government

licences in Northern Ireland (and Scotland) conditional on Applicants

completing checks that they confirm they are appropriately registered for tax

(this legislation already exists in England and Wales).

Contained in the ‘other consultations’ section is a consultation

dealing a review of aviation tax, with a potential reduction in air passenger

duty for intra UK flights (i.e. Belfast to GB) being financed by an increased air

passenger duty on longer international flights. There is a consultation on a

new tax on the largest residential property developers with a view to such tax

helping to pay for the costs of cladding remediation. There is a publication of

the review of the taxation of trusts which is indicating that no major changes

are likely ‘at this stage’ and there are consultations on the aggregates levy

and landfill tax. There is a report on the consultation in respect of the

requirement for large businesses to notify HMRC of uncertain tax treatment (this

reporting requirement is now delayed until April 2022). There are also several

reports on previous VAT consultations covering: VAT grouping (as a result of

which no changes are to be made to the current rules); VAT partial exemption

and the prevention of value shifting of VAT in respect of multicomponent goods

with different VAT rates. There are also consultations to simplify the

maintaining of transfer pricing documentation and on the options to clarify and

update the rules in respect of securitisation vehicles.

So what was not subject to a consultation in today’s

publication? Somewhat surprisingly capital gains tax was not mentioned, despite

two Office of Tax Simplification (‘OTS’) reports last year which looked at potential

major changes to the capital gains tax regime. Similarly, whilst there were

some proposed simplifications to the inheritance tax reporting regime, there

was no consultation on the determination of inheritance tax, again despite an

OTS report being published in 2019 on this topic. There was however a letter to

the OTS which indicated that “The Government will respond to the

recommendations made in the OTS inheritance tax report on simplifying the

design of inheritance tax in due course”. Whilst no potential changes were

announced today, it would appear that this issue has not gone away! So the good

news is that there should still be time for tax efficient estate planning

strategies to be implemented.

Fortus Group Holdings (‘Fortus’), the UK and Ireland’s value added B2B security distributor, has announced the acquisitions of Enterprise Security Distribution and remote CCTV monitoring specialist RE:SURE. These transactions effectively double the size of Fortus to 100m euros in revenue.

Fortus was supported in terms of financing for these transactions by AIB Corporate Banking (Dublin) led by Conor Brogan; and Rockpool Investments (London) led by Guy Ellis.

Fortus was advised by: Eversheds Sutherland led by Tony McGovern (Legals – Corporate & Banking), PKF Francis Clarke led by Sam Phillips (Financial & Tax Due Diligence – Enterprise) & HNH Partners led by Rodney McCaughey (Financial & Tax Due Diligence – Re:Sure)

Enterprise Security Distribution (‘Enterprise’):

Enterprise, founded in 1992, is a UK supplier of security products to installers. The company has nine locations – Sheffield, Birmingham, Kent, Bristol, Manchester, Nottingham, Bedford, Bramley and Norwich – and employs about 90 staff, and has a customer base of 8,000 customers. The leadership team across the nine branches will remain, and will become members of the Fortus Leadership Team.

Fortus describes the business as a great fit in terms of its customer centric culture. Through this acquisition Fortus expands its footprint through full ownership of nine branches, as well as gaining access to new products through their supplier distribution agreements.

Re:Sure Intelligence Ltd:

Re:Sure Intelligence Ltd is a specialist remote CCTV monitoring service serving clients across Ireland and the UK. The company was established in 2007 with the aim of providing a CCTV service that prevents crime rather than just recording it, in a cost-effective manner. It is and will continue to be led by John McMahon (Managing Director) and Emmet Hogan (Commercial Director) who retain a significant stake in the business. The RE:SURE management team will also remain, and the company will continue to conduct business-as-usual with its service and product offerings. The business has the main Alarm Receiving Centre in Cookstown, County Tyrone, Northern Ireland with a smaller office in Sandyford, County Dublin.

The business is fully accredited by the SSAIB, the Republic of Ireland regulator the PSA, and NSAI. The plan with Re:Sure is to endeavour to cross sell this value-add service to customers following the acquisition of Enterprise.

Brian Honan, Founder and CEO of Fortus, said: “Upon completion of both deals, Fortus will advance its strategy of becoming the largest security and fire supply chain business in the UK and Ireland giving us the ability to offer our customers unrivalled support, expertise and monitoring solutions. With our supplier offering, branch network, CCTV expertise combined with RE:SURE’s best in breed monitoring solution, our end-to-end offering will be a first within the security market. We are delighted to welcome the outstanding Enterprise and RE:SURE teams to Fortus Group.”

Mark Brophy, CFO at Fortus said: “These transactions represent a pivotal moment in the evolution of Fortus into the most cutting edge and forward thinking business in the security supply chain sector. We are proud to enjoy the continued support of Rockpool Investments and AIB Corporate Banking to allow us execute our buy & build strategy across the UK and Ireland.”

And Mark Massie, Commercial Director UK, pictured, said: “The acquisition of ESD and RE:SURE is significant news within the security and fire industry. It provides Fortus with a branch foothold across England and opens channels for us to supply our customers with additional industry leading brands, including Fire as well as offering additional services to our customers. I’m delighted to welcome the ESD and RE:SURE team to Fortus Group.”

In his second Budget, the Chancellor focused on three main areas – supporting business and people; fixing the public finances; and building the future economy. The total government support programme for the last fiscal year and this coming year, the detail of which was contained in the first part of the Budget speech, will have cost over £400 billon. The impact of this supercharged public expenditure on the national debt has been enormous and will continue to be so for decades to come. Unsurprisingly, the second part of Mr Sunak’s speech turned to the daunting task of what to do about this debt, which is soon going to peak at almost 100% of national income. Having discounted doing nothing, cutting public expenditure or raising income tax or VAT rates, the Chancellor announced that most tax reliefs and exemptions would be frozen until at least 2026 and that the corporation tax rate for large companies would rise to 25% in two years’ time. In the third and final part of his speech Mr Sunak announced incentives to encourage capital investment by businesses, continued short term stamp duty help for house buyers and a short term continuation of a reduced VAT rate for the hospitality industry. There was no mention of a further Budget later in the year but given the scale of the fiscal issues caused by the Covid 19 pandemic, it would not be surprising to see the Chancellor back on his feet with additional fiscal measures before Christmas.

Some of the key

tax-related points are set out below:

Capital Gains Tax (“CGT”) and Inheritance Tax (“IHT”) – there have been no changes to the headline rates or reliefs for either CGT or IHT. Business Asset Disposal Relief remains available for CGT purposes for total qualifying lifetime gains of up to £1m, while Business Property Relief for IHT is also unchanged. The IHT nil rate band will continue at £325,000 from 6 April 2021 until 5 April 2026.

Income tax allowances and thresholds – the personal allowance, basic rate limit and higher rate threshold will all increase with effect from 6 April 2021 as previously announced, to £12,570, £37,700 and £50,270 respectively. Thereafter, these allowances and limits will be frozen (i.e. with no further CPI increase) until 5 April 2026.

Increase in corporation tax rate – the main rate of corporation tax for will increase from 19% to 25% with effect from 1 April 2023.

Corporation tax small profits rate – a small profits rate of corporation tax of 19% will be introduced from 1 April 2023 for companies with profits of £50,000 or less. Companies with profits between £50,000 and £250,000 will be taxed at 25% but will be able to claim marginal relief. These thresholds are proportionately reduced for the number of associated companies and for short accounting periods.

Use of trading losses – companies and unincorporated businesses will be able to carry back trading losses of up to £2m per annum incurred in the years ended 31 March 2021 and 2022 for a period of three years rather than one year. This should facilitate tax refunds for formerly profitable businesses temporarily hit by the lockdown.

Capital Allowances – the Annual Investment Allowance of £1m has been extended to 31 December 2021.

Super deduction for qualifying plant and machinery – from 1 April 2021 to 31 March 2023, fixed asset investments qualifying for main rate capital allowances will be relieved by an enhanced temporary 130% first year allowance or “super deduction”. Investments in capital assets which qualify for special rate relief, will be eligible for a 50% first year allowance.

Pension Lifetime Allowance – similarly, the standard Lifetime Allowance for pensions will be frozen at £1,073,100 from 6 April 2021 to 5 April 2026.

Stamp Duty Land Tax nil rate band – the increase of the nil rate band for residential property in England and Northern Ireland to £500,000 will be extended from 31 March to 30 June 2021. It will then reduce to £250,000 from 1 July to 30 September 2021, and then to the standard amount of £125,000 from 1 October 2021.

VAT for tourism and hospitality – the temporary reduced rate of VAT (i.e. 5%) for hospitality, holiday accommodation and attractions will also be extended for 6 months to 30 September 2021. It will then increase to 12.5% from 1 October 2021 to 31 March 2022, after which it will return to the standard rate of 20%.

Research and Development (“R&D”) tax relief – for accounting periods beginning on or after 1 April 2021, the amount of SME payable R&D credit that a company can receive in any one year will be capped at £20,000 plus 3 times the company’s total PAYE and NIC contributions.

Freeports – a number of ‘Freeport’ tax sites will be created at various locations around the UK, allowing businesses in these tax sites to benefit from a number of tax reliefs. Eight Freeport sites have been announced in England, and the Government will consult with the devolved administrations on its intention to create similar sites in Northern Ireland, Scotland and Wales.

It gives us great pleasure to announce some promotions and exam successes within HNH despite continued lockdowns and a somewhat abnormal working environment.

Thomas Horner has been

promoted to Manager within our Business Advisory Services (BAS) team and Killian

Kiernan has also been promoted to Assistant Manager within the Forensic

Services department.

James Neill, Head of BAS,

commented:

“The hard work and dedication

of both Thomas and Killian has been evident from the moment they joined the

firm. Thomas has transitioned seamlessly into the BAS department and his

banking experience adds to the skillset within the team, whilst Killian has

been and continues to be instrumental to the growth of the HNH Forensic offering.

We are delighted to see them

both progress their careers in HNH and further strengthen our client offering.”

In further good news, Jamie

Callaghan, also in our BAS department, has successfully passed his Certified

Proficiency in Insolvency (CPI) exam with distinction.

It caps a strong period for

Jamie who not only became our first trainee to complete his training contract and

become a qualified Chartered accountant, but also was promoted to Assistant

Manager last March.

“Jamie’s recent successes are

a credit to him. The distinction obtained in his CPI’s is no less than he

deserves and I look forward to continuing to watch Jamie develop and grow within

the firm.

In the uncertain times that we

continue to experience, these achievements should not be overlooked and we

would like to offer our thorough congratulations to Thomas, Killian and Jamie.

After a

one-year delay due to the impact of the Covid-19 pandemic, changes to the OPW

rules (sometimes referred to as “IR35 rules”) for the private sector are

finally coming into force with effect from 6 April 2021. This will bring the

private sector substantially into line with rules which have been applied to

the public sector since 6 April 2017.

Broadly, the

OPW rules apply to situations where individual contractors or consultants (referred

to as “workers” below) provide their personal services to client organisations

(usually companies) through an intermediary (usually their own ‘personal

service companies’ or “PSCs”). The supply chain can also sometimes involve agencies.

Under current rules for the private sector, if a hypothetical contract between the

individual worker and the client would be a deemed employment relationship for

tax purposes, the PSC is required to

account for PAYE and NICs on the payments that it receives under its contract

with the client. It is currently the PSC’s responsibility to determine the

deemed employment status of the individual worker and pay over any PAYE/NICs to

HMRC. The client currently has no obligations with respect to PAYE/NICs in

respect of payments to workers via their PSC or intermediate agents.

For payments

made on or after 6 April 2021, the responsibility for determining the deemed

employment status becomes that of the client, and the responsibility for accounting

for PAYE and NICs (and, if applicable, apprenticeship levy) on payments to the

PSC will become that of the party which makes the payment to the PSC (the ‘fee

payer’). Where there are no other parties in the contractual chain between the

client and the PSC, the client will be the fee payer and will thus have

responsibility for deducting PAYE and NICs and accounting for same to HMRC.

Therefore, with effect from 6 April 2021, clients’ responsibilities will be significantly increased, and will include the following:

Carrying out a status determination

The

client must carry out a status determination in respect of any worker who

provides their services to the client through an intermediary. The client is

required to take ‘reasonable care’ when carrying out such a determination. The

determination of employment status is not straightforward and is based on a

number of different factors including control, personal service, financial risk

and mutuality of obligation.

HMRC

has developed a tool (the ‘Check Employment Status for Tax’ or ‘CEST’ tool) to

help organisations to determine employment status. It should be noted that

there are some instances where CEST will not come to a formal determination,

and indeed the Courts have, on occasion, disagreed with a CEST result (although

HMRC significantly enhanced the tool in November 2019, to provide a greater

degree of accuracy). Given that HMRC has stated that, provided the questions in

CEST are answered accurately and in accordance with HMRC guidance, they will

stand over the CEST result, it is at least a good place to start when looking

at employment status.

Delivering a Status Determination Statement (“SDS”)

The client must

deliver an SDS to the worker and also to any third party that the client

contracts with. This SDS must set out the reasons for the status determination.

There is no set format for such a statement although HMRC has stated that if

the CEST output is delivered, they will regard this as constituting a valid SDS,

provided the CEST questions have been answered accurately and in accordance

with HMRC guidance. The SDS must be delivered by the client before any payment

is made.

Establishing a disagreement process

This is to allow

workers to challenge the status determination, if they so wish. Where a worker

makes such a challenge, the client is required to respond to the worker within

45 days either with reasons why it does not agree with the challenge or to

provide a new SDS on the basis of the worker’s representations and state that

the previous SDS is withdrawn.

Accounting for PAYE and NICs

Where the client

is also the fee-payer, it must deduct and account for PAYE and NICs (and, where

appropriate, apprenticeship levy) to HMRC in respect of payments made to the

PSC.

There is an

exemption from the new OPW rules for ‘small’ client businesses, such that the responsibility

for determining status and accounting for PAYE and NICs remains with the PSC.

In order to be small, a business will need to satisfy two or more of the

following requirements:

1) It has an annual turnover not exceeding £10.2m

2) It has a balance sheet total not more than £5.1m

3) It had an average of no more than 50 employees for the company’s financial year.

There are

specific rules for businesses becoming or ceasing to be small, and also for

unincorporated businesses. Specific advice should be taken regarding whether,

and when, the ‘small’ business exemption will apply.

It should be

noted that the changes to the OPW rules do not change the criteria for

determining employment status for tax purposes, and it should also be

emphasised that deemed employment status under the OPW rules applies for tax

purposes only. Legal advice should always be taken in order to determine an

individual’s position – and an organisation’s responsibilities – for the

purposes of employment law.

If you have any

queries about how the forthcoming changes to the OPW rules will affect your

organisation, please contact Eamonn Donaghy, Mark Hood or June Barton to

discuss further.

James Neill and Cathy McLean are delighted to be presenting

to the Law Society of NI this Wednesday as part of their CPD programme.

They will be discussing the various changes we are witnessing across our advisory practice including current market trends, updates within forensic accounting, the introduction of new insolvency legislation and the widespread support available to firms.

A double helping of good news today as we announce two new additions to Deal Advisory and Transaction Services and congratulate two existing team members on their promotions.

Paul Gleghorne has been promoted to Associate Director in our Deal Advisory Team and will take the lead on engagements in the waste, energy and renewables sectors in addition to continuing his leadership role within financial modelling engagements. Peter Graham has been promoted to Senior Manager in our Deal Advisory team.

Duncan Thorburn joins our Deal Advisory team in Edinburgh as a Senior Manager from a similarly-positioned M&A boutique in Scotland, where he has been working across both corporate finance and TS for the last five years. He was previously at RBS, having joined their graduate scheme and fulfilled a number of customer facing and internal reporting roles.

Duncan arrives with strong experience and insight into the Scottish Tech sector and the wider SME funding environment, and we recently worked in conjunction with him when he undertook a buyer diligence role for Maven on Quorum Cyber, the MBO HNH advised on in June 2020.

Harry Linklater, Deal Advisory Director for Scotland, welcomed Duncan to the team, saying , “We believe that adding Duncan into the fold at HNH will be a key strategic addition to our team in Scotland, bolstering the ability we offer to provide experienced and relevant input to the technology and wider market here at HNH. Our focus has always centred on delivering best in class advice at a senior level, with an emphasis on local clients and Duncan’s addition enhances that’.